Vietnam Merger Control: Is Merger Filing Required For “Top-Up” Acquisitions?

This update discusses viewpoints on whether atop-up acquisition (where the purchaser already has control over the target company) is subject to the merger filing requirement in Vietnam. The position of the Vietnam Competition Commission (“VCC”) in a recent filing offers welcome clarity.

Recap of regulations and legal issues

Under the Vietnamese competition law, a contemplated transaction must be notified to the VCC if (i) it qualifies as an economic concentration, and (ii) a relevant statutory threshold(e.g., assets, revenues, transaction value, or combined market share) is met.

For the first test, an acquisition would be considered an economic concentration if “the purchaser (directly or indirectly) acquires all or part of the charter capital or assets of another company sufficient to control the acquired company or one of its business lines” (Article 29.4 of the Competition Law 2018,emphasis added). “Control” in this context includes (i) holding more than 50% of the voting shares or charter capital of the target company;(ii) holding more than 50% of the target company’s assets in all or one of its business lines; or (iii) holding decisive rights over the target company’s corporate governance or important business matters (Article2.1 of Decree 35/2020/ND-CP).

As an illustration, consider a contemplated transaction where the purchaser does not yet own any equity in the target company and intends to acquire 80% of the target company’s charter capital. In this scenario, since the acquisition confers on the purchaser control over the target company which it did not previously have, the acquisition qualifies as an economic concentration and must be notified to the VCC if any relevant statutory threshold is met.

Now is situation and the question:

If, following that transaction, the purchaser undertakes a “top-up” acquisition to increase its interest in the target company from 80% to 90% (the “Top-up Acquisition”), would the Top-up Acquisition qualify as an economic concentration, thus trigging merger filing obligation, under Vietnamese competition law?

We have observed two approaches on this matter:

(a)Approach 1 – No change of control (not notifiable):

Since the purchaser already controls the target company (by holding more than 50% of the charter capital) and the Top-up Acquisition does not alter that control, the transaction does not constitute an economic concentration (in the form of an acquisition or otherwise). Therefore, the Top-up Acquisition does not trigger a merger filing obligation in Vietnam.

(b)Approach 2 – Additional control (potentially notifiable):

Based on the language of Article 29.4 of the Competition Law 2018, there is arguably an interpretation that, regardless of the purchaser’s pre-existing control over the target company, a transaction that results in the purchaser’s post-transaction ownership ratio exceeding 50% can still be viewed as an additional acquisition of charter capital “sufficient” to control the target company. Under this view, the Top-up Acquisition would be treated as an economic concentration (in the form of an acquisition) and, if any relevant statutory threshold is met, a merger filing would be required.

In the absence of formal guidance from the competent authorities on the notifiability of Top-up Acquisitions, it remains uncertain whether parties should forgo a merger filing and accept the non-filing risk, or, more prudently, allocate time and resources to file for compliance.

In a recent filing we assisted our clients, the VCC set out its approach to a Top-up Acquisition on a case-specific basis.

Case background

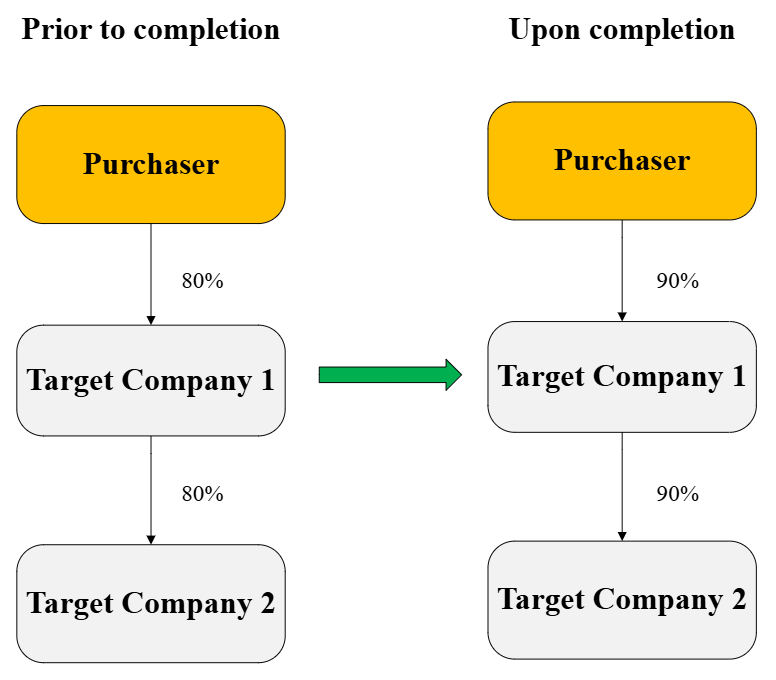

The Purchaser, a foreign-invested enterprise, directly holds 80% of the charter capital of the first target company (“Target Company 1”), which in turn directly holds 80% of the charter capital of the second target company (“Target Company 2”) (collectively, the “Target Companies”). The Purchaser proposed the following two-step transaction (the “Contemplated Transaction”):

Step 1: The Purchaser would subscribe for new shares representing an additional 10% of Target Company1’s charter capital, increasing its direct holding from 80% to 90%.

Step 2: Target Company 1 would then acquire an additional 10% of Target Company 2 ’s charter capital,

increasing its direct holding in Target Company 2 from 80% to90%.

Upon completion, the Purchaser would directly hold 90% of Target Company 1 and in turn Target Company 1 would directly hold 90% of Target Company 2.

The aggregate assets in Vietnam of the Purchaser and its affiliated group (including the Target Companies)exceed VND 3,000 billion. Accordingly, if the Contemplated Transaction (i.e., the top-up from 80% to 90%) constitutes a statutory acquisition under Article29.4 of the Competition Law 2018, it would trigger a merger filing obligation.

Given the lack of official guidance and to manage the mis-filing risks, a filing was submitted.

The VCC’s decision

The VCC was of the view that the Contemplated Transaction was not subject to a merger filing obligation for the following reasons:

(1)At the time of notification, the Purchaser directly held 80% of Target Company 1, and through Target Company1, indirectly held 80% of Target Company 2. Therefore, the Purchaser already had control over the Target Companies under Article 2.1 of Decree 35/2020/ND-CP; and

(2)The increase in ownership from80% to 90% would not change the Purchaser’s controlling rights over the Target Companies. Therefore, the Contemplated Transaction does not qualify as a statutory acquisition under Article 29.4 of the Competition Law 2018, and thus does not trigger any merger filing obligation.

Key takeaways

The VCC’s view on the notifiability of the Contemplated Transaction indicates (on a case-specific basis)that a top-up acquisition would not qualify as a statutory concentration under Article 29.4 and not trigger merger filing obligation if (i) the purchaser already holds more than 50% interest in and has control over the target company, and (ii) the transaction does not alter the purchaser’s control.

The VCC’s decision may not constitute a guidance; it applies specifically to the Contemplated Transaction only. Nevertheless, the approach in this case should be a useful reference point, hopefully signalling a positive movement toward comparable top-up acquisitions.