With strong government backing, finance continues to dominate the jurisdiction’s venture capital landscape but more clarity around licensing in burgeoning areas such as crypto and better assistance for business matching are needed to help startups scale.

Hong Kong’s venture capital (VC) landscape has ample growth opportunities but improvements in licensing, talent attraction and business matching will be keys to success.

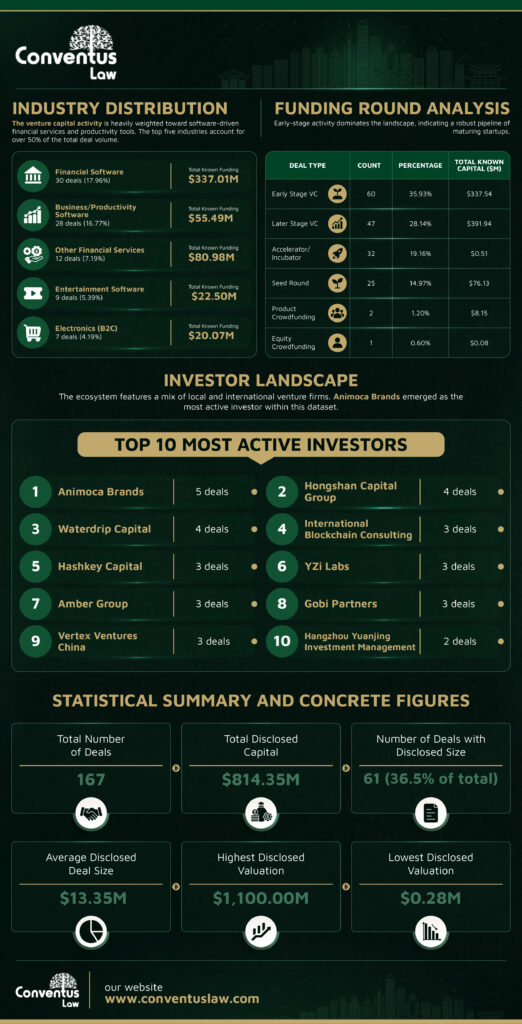

Based on Morningstar data* analysed by Conventus Law, Hong Kong’s VC activity in 2025 was dominated by the financial sector.

Out of a dataset of 167 transactions, 30 financial software deals (18%) accounted for $337 million in funding, followed by business and productivity software with 28 deals (17%) at $55.5 million and financial services with 12 deals (7%) at $81 million.

The most active investors included Animoca Brands (5 deals), Hongshan Capital Group (4 deals), Waterdrip Capital (4 deals), International Blockchain Consulting (3 deals), Hashkey Capital (3 deals), YZi Labs (3 deals), Amber Group (3 deals), Gobi Partners (3 deals) and Vertex Ventures China (3 deals).

“For firms focused on cutting-edge sectors, more detailed clarity is essential to navigate the landscape effectively,”

Mia Mai – HashKey Capital

According to Mia Mai, head of portfolio and ecosystem, and Edward Zhou, senior investment analyst at HashKey Capital, Hong Kong has been actively embracing innovation in recent years.

With investments across crypto, artificial intelligence and fintech in more than 600 companies, Hong Kong remains a key investment hub for HashKey Capital, which works with a range of startups, including early-stage and mature-stage companies, as well as emerging talent at local universities looking to commercialise their projects.

Mai noted that Hong Kong regulators have been accelerating the rollout of various frameworks and guidance to support the blockchain industry.

While this momentum is encouraging, public information around some of the new licensing requirements remains relatively limited at this stage.

“For firms focused on cutting-edge sectors, more detailed clarity is essential to navigate the landscape effectively,” said Mai. “Similarly, our portfolio projects that are looking to establish or expand their presence in Hong Kong would benefit from additional guidance to help them settle down and grow locally.”

“Founders that prepare properly tend to have a much smoother fundraising process.”

David Cameron – DCLO

For instance, VC funds investing in the crypto space in Hong Kong need to meet the new licensing requirement under the Anti-Money Laundering Ordinance (AMLO). This is an additional requirement on top of the existing licensing requirements under the Securities and Futures Ordinance (SFO).

More clarity around any overlap between the AMLO and SFO licensing regimes from the regulators would be helpful—along with more detailed public guidance, including transitional arrangements for licence extension, to ensure a smooth rollout.

David Cameron, managing partner of David Cameron Law Office (DCLO), said Hong Kong already has many of the ingredients to become a leading venture capital hub in Asia, including deep capital markets, sophisticated investors and strong connectivity with mainland China.

“Broader supporting system—including company incorporation, banking services, tax incentives and business networks—will also be essential to help startups thrive locally.”

Edward Zhou – HashKey Capital

Cameron noted that the introduction of the Limited Partnerhip Fund (LPF) regime has helped strengthen Hong Kong’s attractiveness as a fund domicile and demonstrated the city’s willingness to introduce commercially practical structures.

“The next step is ensuring that regulation in emerging sectors develops with sufficient clarity and speed so that founders and investors can cooperate with confidence,” he said.

One area where Hong Kong could further strengthen its overall support for the blockchain industry is talent attraction.

“While the city has ample talent in traditional finance, there remains a shortage of Web3 talent, particularly product managers for funds,” said Zhou. “Broader supporting system—including company incorporation, banking services, tax incentives and business networks—will also be essential to help startups thrive locally.”

While Hong Kong offers good support for business incubation, there’s a gap in helping businesses scale.

Ankit Suri

An analysis of the data obtained by Conventus Law reveals that more than half of the VC deals in Hong Kong in 2025 involved early and late stage VCs, demonstrating their importance in attracting funding and the need to provide support for these businesses.

Out of the 167 VC transactions in 2025, early stage VCs accounted for 60 deals (36%) at $337.5 million while later stage VCs made up 47 deals (28%) at $391.9 million.

Ankit Suri, former CEO and co-founder of fintech firm Planto who is now building and advising on AI ventures in financial services, said that compared to 2018 when he founded Planto, the VC landscape in HK has become more challenging.

“Investors are demanding more from entrepreneurs and founders are taking longer to raise seed rounds,” he said. “While Hong Kong offers good support for business incubation, there’s a gap in helping businesses scale.”

Scale or Fail: The Hong Kong Growth Playbook

His recommendations are to provide better support for business matching with VCs, encourage more risk capital flows particularly from family offices and ultra high net worth individuals, support more M&A activity between corporates and startups, as well as bolster accelerator related activities.

Cameron said one of the key challenges for startups in Hong Kong is scaling beyond the incubation phase.

“We regularly help clients prepare for capital raises by cleaning up cap tables, formalising shareholder arrangements, reviewing employee incentive structures and generally getting businesses into a position where they are ready for institutional investment,” he said. “Founders that prepare properly tend to have a much smoother fundraising process.”

While Hong Kong’s VC landscape is attractive to investors, more regulatory clarity in burgeoning sectors, targeted talent attraction measures and support in business and capital matching will be essential for the industry’s growth.

*The Morningstar data obtained had a high rate undisclosed financial information, including missing deal sizes, valuations and demographic data. The absence of this data limits the ability to calculate the true total market capitalisation and a granular analysis of valuation trends. However, based on statistical extrapolation of known data points, the estimated total deal capital for undisclosed transactions was estimated to be $2,229.45 million.