23 March, 2019

Introduction

Following the introduction of a range of new asset management regulations that came into effect last year (the “New Asset Management Regulations”), the implications are starting to emerge for the whole asset management industry, including a wide range of asset managers, such as banks, securities companies, fund management companies and insurance companies.

The New Asset Management Regulations’ ban on the multi-layered nesting of asset management products has exposed the need for an alternative method of facilitating business collaborations among various types of asset management institutions.

Recently, the China Securities Regulatory Commission (CSRC) solicited public comment on the Guidelines for Manager of Managers’ (MOM) Products for Securities Fund Business Institutions (the “MOM Consultation Paper” or “MOM Guidelines”).

As the first set of guidelines directed at the management of MOM products within the overall asset management industry, the MOM Consultation Paper comprises various important elements:

I. Definitions and Legal Relationships of MOM Products

1.1 Definition

The MOM Consultation Paper defines MOM products as those products for which a securities and fund business institution, as a manager (a “parent manager”), delegates, whether partially or entirely, the fund assets to a small number of qualified, third-party asset management institutions (“sub-managers”) in order to manage the investment. Various implications can be drawn from this definition:

(1)The MOM products regulated by these Guidelines only refer to those issued by securities and fund institutions regulated by the CSRC, such as securities companies or their securities asset management subsidiaries, and mutual fund management companies or their subsidiaries. It is unclear whether the CSRC will introduce similar guidelines governing futures asset management institutions or private fund managers, based upon the MOM Guidelines.

In addition to the MOM products regulated by the CSRC, those bank and insurance asset managers under the regulation of China Banking and Insurance Regulatory Commission (CBIRC) may also issue MOM products as well, and hence we expect that the CBIRC may at some point separately formulate its own MOM product regulations.

(2)The MOM Guidelines refer to “diverse assets and multiple managers”, with the implication that an MOM product is required to have more than one sub-manager. We note that the Consultation Paper does not mention the maximum number of sub-managers nor any requirements as to how the managed assets for a single MOM product should be allocated.

(3)The Consultation Paper indicates there may be some flexibility in asset allocation, allowing for an MOM parent manager to either delegate the entire managed assets to sub-managers, or to choose to keep a portion of the assets under its own management.

1.2 Legal Relationship

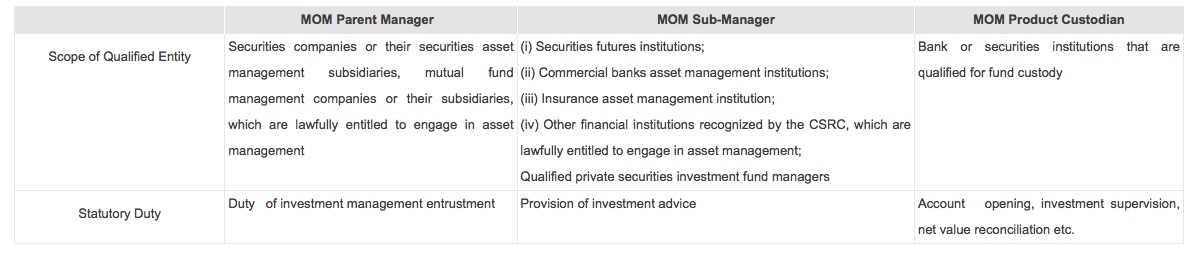

The legal status and duties of the relevant parties involved with MOM products are listed in Table 1.

Table 1

Please click on the table to enlarge

These definitions suggest that almost all asset management institutions would currently qualify as sub-managers. These would include asset management institutions of securities, mutual funds and futures, private securities investment fund managers (though private equity investment fund managers are excluded), and also those bank and insurance asset management institutions not regulated by the CSRC. As such, the Guidelines allow for the selection to be made from a broad range of sub-managers, and thereby provide the opportunity for diversified asset allocation. With “other financial institutions recognized by the CSRC” also included in the scope of qualified sub-managers, it is possible that trust companies may in the future also be able to act as sub-managers.

It should be noted that an MOM parent manager and sub-manager are not deemed as “co-trustees”. Rather, they have an “principal-agent” relationship, with the MOM parent manager being the sole manager of an MOM product, while the sub-manager, in substance, acts as a servicing institution providing investment advisory services. The MOM Consultation Paper stipulates that an MOM parent manager’s legal obligations are not discharged just because it has entrusted management of the relevant assets to sub-managers, and at the same time emphasizes that a sub-manager shall be liable for its own violations.

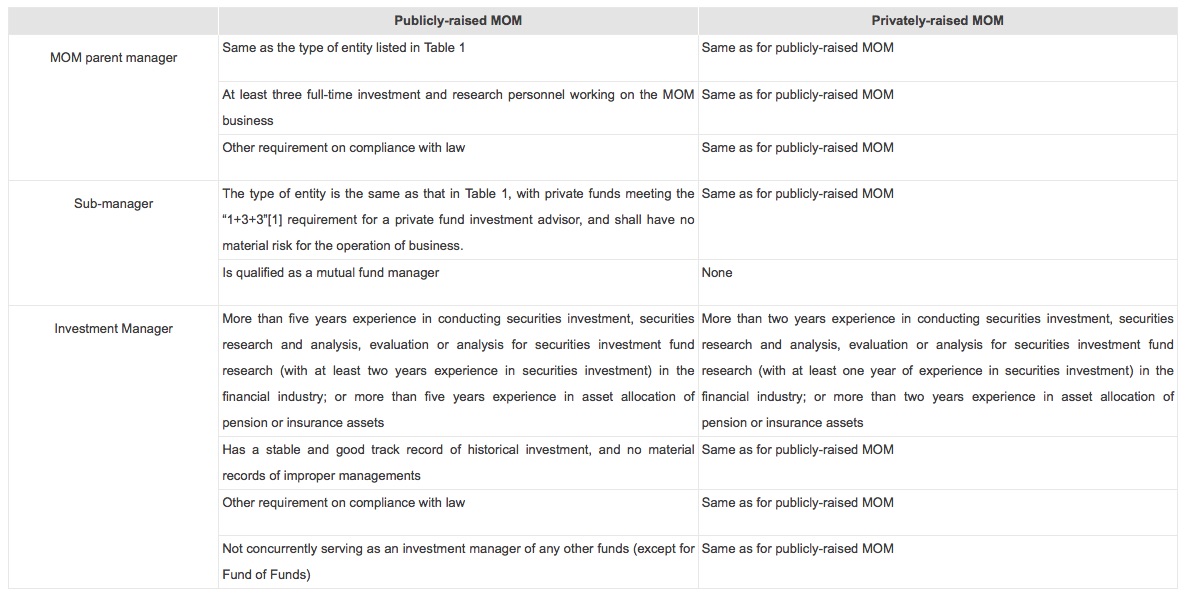

II. Setting Different Qualification Requirements on Managers for Publicly and Privately Raised MOM Products

The MOM Consultation Paper indicates that an MOM parent manager can issue both publicly-raised and privately-raised products, and that the relevant qualifications for each should be met by both the parent and sub-managers, as below in Table 2.

Table 2

Please click on the table to enlarge

III. MOM Parent Manager's Duties

3.1 MOM Parent Manager’s Management Duties

As the sole manager of an MOM product, an MOM parent manager shall strictly perform all the duties of a manager of MOM products, including but not limited to determining the product investment strategy and the investment strategy authorization mechanism, dividing sub-asset units and separately valuating and verifying each sub-asset unit, being responsible for the ultimate investment decision about and trading execution of MOM products, having overall risk control and compliance management for the products, keeping traceable records of the trading execution of each sub-asset unit, preparing information disclosure documents for an MOM product, and so on.

3.2 MOM Parent Manager’s Supervisory Duties

The Consultation Paper clearly outlines the duties of an MOM parent manager in terms of supervising sub-managers, namely that an MOM parent manager shall reasonably determine the number of sub-managers and the scale of assets managed by each sub-manager, establish reasonable mechanisms and procedures for the appointment, engagement, evaluation, and replacement of sub-managers, conduct due diligence on sub-managers, continuously supervise and assess sub-managers’ management of assets, and make regular return visits, the frequency of which shall be no less than once a year and which should include activities such as the record-filing of sub-managers.

As per the compliance requirements prescribed in the New Asset Management Regulations on the engagement of investment advisors, sub-managers for MOM products are only able to provide investment advice, and should not make the ultimate investment decisions or execute trades, both of which are only to be exercised by MOM parent managers. Responsibility for the monitoring of the implementation of the relevant investment instructions falls under the overall risk detection of the MOM parent manager.

The MOM Consultation Paper prohibits a sub-manager from sub-delegating their duties. It also requires the MOM parent manager to establish monitoring mechanisms for any relevant transactions, to supervise all related parties of sub-managers, and to take steps to avoid any conflict of interest. The Consultation Paper very plainly forbids an MOM parent manager from engaging sub-managers who are related parties, though, pursuant to Article 19, it does not prohibit an MOM parent manager from engaging its own affiliate as a sub-manager, so as long as this is disclosed. We are of the view that it is likely, in practice, that an MOM parent manager may engage other asset management institutions within its own group to serve as sub-managers. Given that the ban on sub-managers being related parties is likely to impede the development of MOM business opportunities, we would recommend that rather than prohibiting sub-manager related party relationships, it would make more sense to prohibit cross-trades between the sub-asset units.

IV. Detailed Investment Operations

The MOM Consultation Paper provides the following detailed information on the investment operation of MOM products:

(1)Account Opening. Each sub-asset unit shall unilaterally open a securities or futures sub-account in accordance with the regulations.

(2)Scope of Investment. While the MOM Consultation Paper does not specify the scope of investment, on the basis of the provision that only a private securities investment fund manager is allowed to serve as a sub-manager, it could be inferred that the scope of trading will be limited to the trading of securities, futures or other standardized financial instruments. This matter requires further clarification by the CSRC.

(3)Investment Limits. The MOM Consultation contains no explicit ruling about investment limits. It is our understanding that any investment limits that apply will depend upon whether such product is publicly or privately raised, and upon the underlying assets of investment of each sub-asset unit.

(4)Requirement of Record-filing. A sub-manager for a publicly-raised MOM shall record-file with the CSRC; while a sub-manager for a privately-raised MOM shall record-file with the Asset Management Association of China (AMAC).

(5)Sub-manager Service Fee. The basic underlying principle is that any service fee paid by an MOM parent manager to a sub-manager shall be comparable to the services provided by that sub-manager. In order to avoid double charging, the fees charged by a sub-manager for a publicly-raised MOM shall be paid exclusively from the management fees charged by the MOM parent manager. However, there is more flexibility when it comes to a privately-raised MOM, with any such fees being open to agreement between the MOM parent manager and the sub-manager. Based on our understanding, fees for a privately-raised MOM could be paid either from the management fees charged by the MOM parent manager or from a sub-unit’s fund property.

(6)Information Disclosure. AN MOM parent manager shall provide a detailed list of a product’s core elements in the asset management contracts and in other legal documentation, such as the investment arrangement of the MOM, the allocation criteria of sub-asset units, and the standard for selecting sub-managers. The MOM parent manager shall disclose in regular reports any relevant information, such as the basic information about and any changes to each sub-manager, the scale and proportion of assets managed by each sub-manager, any related party relationships between the MOM parent manage and the sub-managers, and disclose in an annual report the sub-manager’s aggregate service fees received for the current year, and the proportion of the fee of the net value of fund assets. It is our opinion that, for service fees paid through the management fees of the MOM parent manager, it will not be necessary to separately calculate and then disclose in the annual report the proportion of service fees of the net value of fund assets.

(7)Risk Warning. An MOM product shall have its name explicitly include the word “manager and managers (MOM)”, and the MOM parent manager shall prepare the MOM product summary and fully disclose to investors the specific risks of such product.

(8)Technical System. The MOM parent manager shall establish a comprehensive technical system to support the investment operations of the MOM product. According to our understanding, since the MOM parent manager takes on the duties of overall risk control and compliance management of the trading execution of each sub-asset unit and MOM product, there are relatively high requirements for the safety, stability and reliability of its information system. Moreover, any issues relating to the external connection information systems shall also comply with the relevant regulations of the CSRC.

(9)Prohibited Activities. There remains some regulatory concern about the management of MOM products. For MOM parent managers, sub-managers and custodians, in addition to for the usual prohibition of activities such as insider trading, market manipulation, using undisclosed information for trading, embezzlement and misappropriation of fund property and seeking illegal interest for a third party, the MOM Consultation Paper also expressly forbids any behaviors that might facilitate activities aiming to violate the law or to circumvent financial regulation, any commercial bribery that uses fund products, any refund of management fees to investors whether directly or indirectly and the improper use of fund property for unnecessary trading.

Conclusion

In conclusion, the MOM Consultation Paper builds a comprehensive regulatory framework for MOM products. The Consultation Papers cover elements including definitions, legal relationships, qualifications and conditions, business model, investment operation, risk management and internal control. Leveraging the strengths of various types of financial institutions, it provides the legal basis to support collaborations between securities and fund business institutions and other asset management institutions. We expect that the MOM Guidelines will soon be promulgated, and that they will ultimately result in positive, comprehensive outcomes for the asset management industry.

![]()

For further information, please contact:

Natasha Xie, Partner, Jun He

xieq@junhe.com

1. This means that it has been registered with the Asset Management Association of China (AMAC) for more than one year without any record of material violation against any laws or regulations, and has at least three investment management personnel having track records in securities or futures investment management which are traceable and run over three consecutive years, with no records of bad practice.