19 September 2017

Deloitte regularly surveys CFOs in almost 60 nations across Asia, Europe, and the Americas. In the last two years these surveys have shown that executives are increasingly worried not just by traditional risks (such as those stemming from economies and politics), but by new ones too (from disruptive technologies to the likes of cyber and terror attacks). Yet, amid all this uncertainty there are a surprising number of things that can still be planned with confidence. In fact, some of the biggest changes in markets as well as entire economies in the years and decades ahead can be mapped with reasonable likelihood.

The first article in this edition, Ageing Tigers, hidden dragons, set out the two key changes we will witness over the next quarter century, such as surging growth potential in India and a peak in the working age population in China, and the outcome of these changes.

The world is beginning to wake up to the emerging challenge of ageing markets. Yet, in many cases, businesses simplistically assume that the glory days of market growth have passed. It may well be challenging, but that demographic destination isn’t absolute. As Japan’s experience of the past two decades already shows, the future might well be challenging, but the impacts of Asia’s demographic destiny don’t have to be entirely, or even mainly, negative.

This article asks how those on the right side of the changes can maximise potential benefits, and how those challenged by demographic destiny can best rise to the challenge.

How big is the demographic challenge?

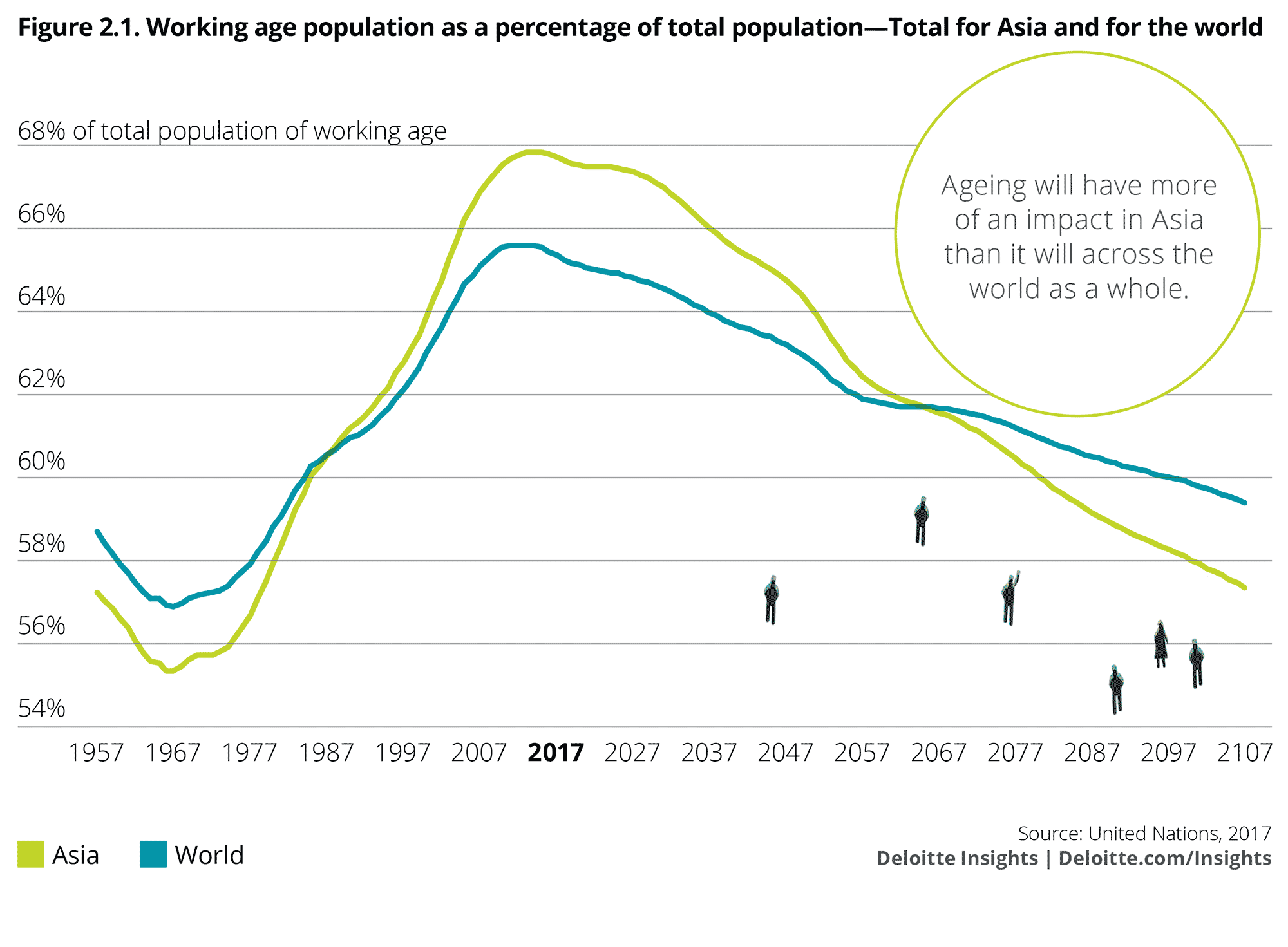

As figure 2.1 shows, agein g is an issue for Asia as a whole, and one that is just about to bite, with more of an impact to be evident in Asia than across the world.

Please click on the graph to enlarge.

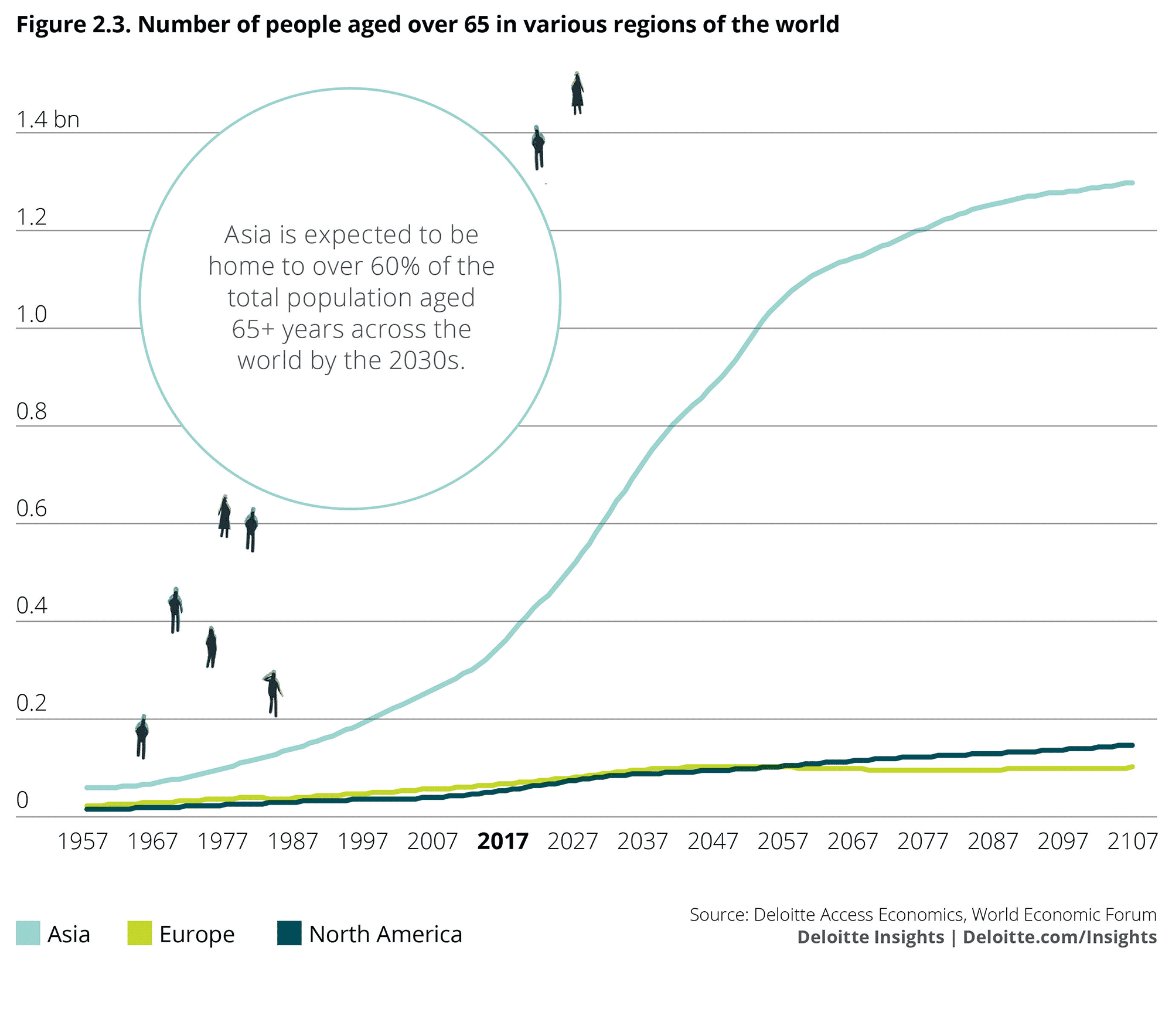

Our analysis shows that those in Asia aged over 65 will be the largest and fastest growing market in the world; they are set to grow in number from 365 million in 2017 to more than 520 million in 2027.

There are already more over-65s in Asia than there are people in all of North America. The number of over-65s in Asia will exceed one billion just after the middle of this century. In fact by 2042 (in just a quarter of a century) there will be more over-65s in Asia than the total populations of the Eurozone and North America combined.

Yes, you read that right: More people aged over 65 in Asia than the total combined populations of North America and the Eurozone, and in just 25 years from now.

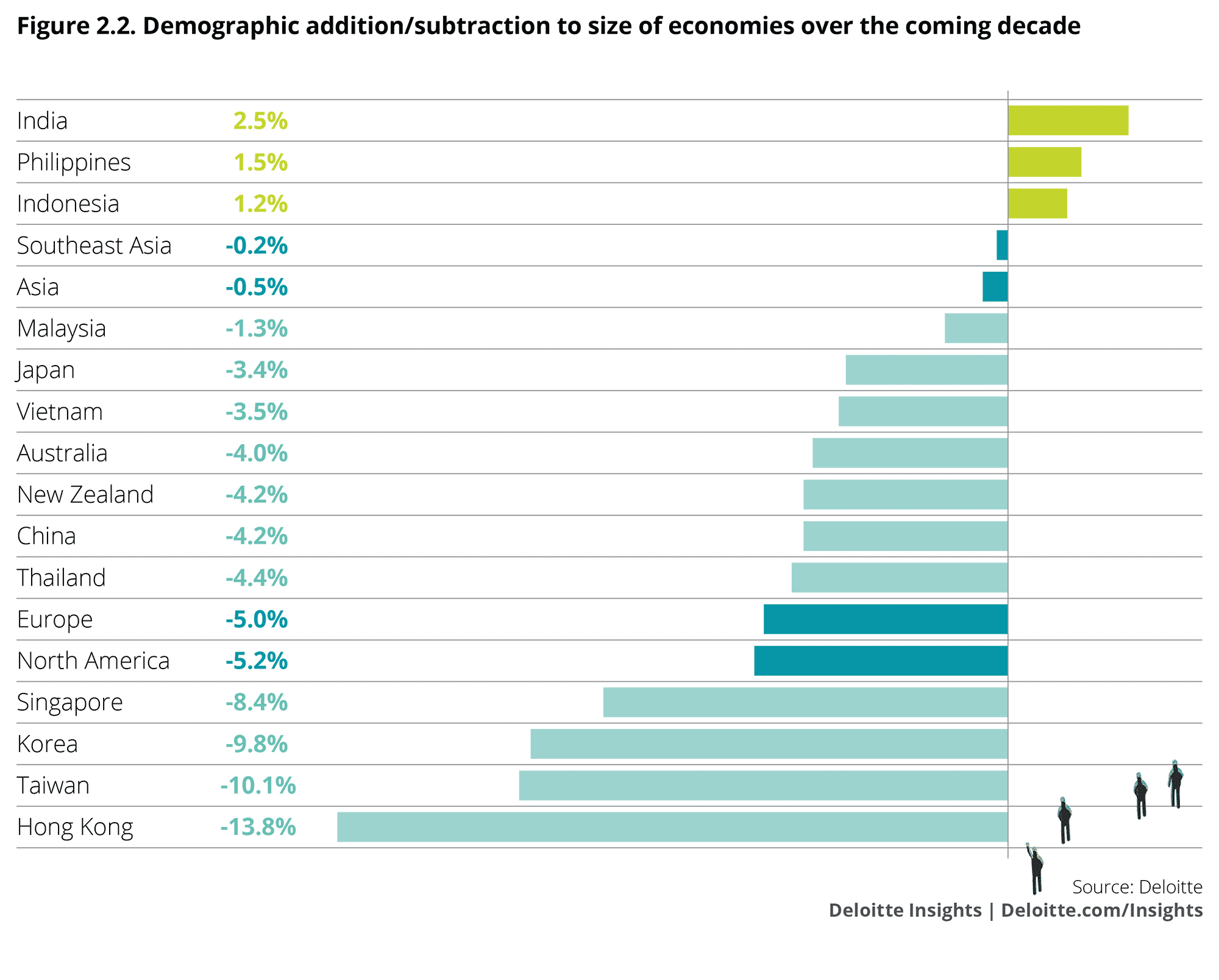

So how big is Asia’s challenge? Figure 2.2 lays out the relative effects of demographic destiny across Asia in the decade ahead.1

Please click on the graph to enlarge.

This figure sets out the demographic dividing line between producers (workers aged 15 to 64) and consumers (the total population). The result is a simple ranking that sheds light on where overall markets will go across the next decade.

But there are factors that would act to both improve and worsen that picture. Why might the effects of ageing be smaller than those shown in figure 2.2?

Retirement age can rise: Not only are people starting work later (as they are studying for longer), but they’re also retiring later. Partly that’s because they can—fewer jobs are back-breaking these days, rising life expectancies are encouraging longer working lives, and today’s higher incomes are also encouraging people to work for longer. Of course, not all people are willing to retire later, but rising life expectancies mean many of them are effectively forced to do so. Many countries are also seeing moves by the government to extend the expected working lives of their citizens to boost their economic potential and mitigate some of the impacts of ageing on public finances.

Accordingly, the assumption behind figure 2.2—that the population aged 15 to 64 is a sufficient proxy for the potential workforce—can overstate ageing effects.

More women could join the workforce: Patterns differ markedly across Asia, but in most nations there are far fewer women than men in the paid workforce. Accordingly, the demographic downdraft to economies can be fought by unleashing the pent up potential among less tapped groups of workers. The potential is significant. As the discussion at the end of this article notes, the potential gains for India can be measured in trillions of dollars.

Migration can give wriggle room: These population projections already assume people moving between nations.

However, if the impact of ageing starts to be too severe, more workers may be ”imported” than these figures allow.

This may be true, for example, for Hong Kong. And it seems unlikely, as these projections would have it, that Japan’s population at the end of this century would have fallen by a third from current levels.

We can actively draw up the experience that comes with age:Much of the evidence shows that the experience older workers can bring to bear on the workplace makes up for any loss of mental dexterity and enthusiasm.

Bigger isn’t necessarily better: In the end, it’s not the size of the economy that determines whether people are happy or not, it’s average incomes and standards of living. This means productivity is just as much a contributor to final outcomes as population and participation. Many previously labour-intensive jobs—ones which might have needed younger workers—may well be replaced by automation in coming years. And governments around the world have long focused on education and skills as a key plank of growth.

And worse isn’t necessarily smaller: As Japan clearly shows, ageing might be challenging, but there are ways to face that challenge. Indeed, across the past decade living standards in Japan have risen almost as fast as those of the United States.

And why might ageing effects be larger than those shown in figure 2.2? First, certain factors mitigate attempts to get around the problem:

Productivity and participation march alongside population:Most importantly, and as noted above, there are both virtuous and vicious cycles in play. Favourable demographics are usually associated with rising workforce participation and better education. While some governments have faced up to the demographic challenge, the world is yet to come to terms with what happens when the demographic pendulum moves onto its downswing.

Migrants age too: Migration can help ward off ageing at the national level, but not forever. Besides, from a global viewpoint, migration is essentially a zero sum game. And in an age of international mistrust, local populations are wary of too many people coming from ”elsewhere.”

Less productivity, less risk-taking: The positives noted above included one about the benefits of experience outweighing ”any loss of mental dexterity and enthusiasm.” But these studies mostly looked at individuals. Once you start to look at states and nations, that’s not what the latest evidence suggests. For example, researchers from Rand Corporation looked at what different speeds of ageing had done to the growth of different states of the United States.2 They found that the direct demographic effects derived in figure 2.2 accounted for less than half the impact of ageing on overall economic growth, as older States became less productive. Although its conclusions were less stark, the International Monetary Fund also found ageing workforces reduced productivity.3

Financial bubbles tend to be formed and burst: When demographics drive growth, an expectation of continuing good growth can get priced into real estate and stockmarkets. Equally, when demographics turn, it can ‘surprise’ businesses, governments and markets, and the resulting failure to meet expectations can see asset prices go through a “bust.”

And then there are additional challenges that ageing will bring:

Budget pressures: In simple terms, governments tax workers and hand subsidies to the young (for their education and health) and the old (for their health and for aged care). So ageing puts stress on government budgets by reducing revenue growth and adding to spending. Other things equal, this weighs on growth because the shortfall has to be remedied by some combination of higher taxes or lower spending.

The rise of the “grey vote”: While the economy in general may be affected by falling growth rates, many will fear that they are being forced to pay too large a price to fix the problem if governments cut expenditures. This may see the increasing electoral voice of the growing older generation stifle much needed policy changes.

On balance then, figure 2.2 may understate the changes afoot across business prospects in a range of nations.

Every challenge is also a business opportunity

Ageing will slow overall economic growth rates in a number of countries, but it will turbocharge a range of specific markets at the same time. Yes, ageing brings costs, but it also brings benefits, and those benefits may be concentrated in particular industries. Simply put, we spend on different things as we age. And therein lies opportunity.

There are megatrends in play here. Across much of Asia:

- We’re getting older.

- We’re getting richer.

- New technologies will add to health care costs.

- Public sector budgets will come under even greater pressure.

- More people will be living with chronic conditions.

This combination says a range of sectors will become bigger business in the future than they are today. And the scale of the opportunities is mind-boggling, with Asia expected to be home to over 60 percent of the total population aged 65+ years across the world by the 2030s. That’s a rapidly rising share of an even more rapidly expanding pool.

As figure 2.3 shows, the number of over-65s in Asia is already much larger than in other regions of the world. This market is set to swell rapidly, hitting almost a billion people by the middle of the century.

Please click on the graph to enlarge.

In fact these markets are already moving. Over the decade to 2027, Asia will see 160 million people added to the ranks of its over-65s. Yet that same figure for the Eurozone and North America combined is just 33 million extra.

That’s not, by the way, to underplay the impact of ageing in the Western world, but to put it in context—Asia is enormous, and it is set to age faster than the West. And, in turn, that says the business opportunities and policy challenges of ageing now loom largest in Asia.

The next decade and more will therefore see a developing ”growth cluster” of health-related businesses across Asia. These business opportunities will lie at the heart of the collision of trends such as rising life expectancies, rising relative health care costs and tightening public sector health budgets.

The last factor is little understood. In most nations, taxpayers fund a larger share of health spending than they do of other types of spending. However, with public sector budgets set to come under increasing pressure over time, more health care and related opportunities will come to the private rather than the public sector.

As the megatrends noted, we’re getting older and richer. That means we are more likely to need health care, and we will also need to pay more for it, but we’ll also be better placed to pay. And technology increasingly means that what we want is actually doable, so more and more procedures are likely to occur.

Of course, some of those advances will cut costs as new drugs will mean surgery is no longer required, or improvements to techniques mean recovery from surgery is much faster and requires less time in hospital.

On the other hand, the world is seeing a shift towards chronic conditions such as diabetes, some types of cancer, dementia, Parkinson’s disease, cardiovascular disorders, and musculoskeletal diseases. And, to the megatrends we’ve just listed, you can also add obesity. With the simple addition of ”heavier” to ”older” there is a risk Asia’s population of diabetes sufferers will surge in the years ahead.

These chronic conditions are likely to be future drivers of health care spending. As Asia lives longer, it is increasingly living with ailments that are not life threatening, but require more care than otherwise.

It won’t just be the case that future conditions will be longer lasting. Many of the new business opportunities they drive will be much more ”recession proof” than average. When times are tough, you may put off buying new clothes or eating at restaurants, but chances are you won’t put off treatment for a sore back or an infected tooth.

Pain is a powerful motivator.

In turn, this points to a welcome advantage for businesses selling into these markets—they know the future looks bright. That’s why the coming wave of growth in health care and related sectors will see a major shift in the spending habits of Asia, presenting a number of business opportunities as it does so.

If ”demographics is destiny,”4 then the future of health and related industries is bright across much of Asia. That very destiny represents a long-term opportunity for businesses to invest in what will clearly be growth sectors in coming decades.

There are policy challenges here too—skilled migrants, anyone?

There are also challenges to be faced, and it isn’t clear whether Asia will rise to these challenges as fast or as fully as it might:

Unlocking people power among female workers: No matter which side of this decade’s demographic divide a nation stands on, it can boost its markets best if it can make the most of its own potential people power. That’s true enough, for example, of Korea, Japan, Indonesia, and the Philippines, where participation rates among women not only lag those of men, but have failed to lift significantly over recent years. It’s even truer for India, where the participation gap is around twice as large as it is in these economies (and has actually widened across this century). Some nations in the region—Australia, New Zealand, Taiwan, Malaysia, Singapore, and Hong Kong—have seen the opposite trend, with female participation rates rising strongly since 2000.5

Welcoming migrants: It makes sense for those nations most at risk of a demographic-driven growth slowdown to be the most open to immigration. Yet, 2017 is a year in which opposition to immigration is garnering votes all over the globe. However, there are some success stories. Singapore, for example, has a low birth rate, but manages a better ranking in the projections here than it would otherwise have done thanks to a relatively liberal view of immigration. Yet, the political willingness to accept migrants often appears to be strongest in regions where, at least from the viewpoint of demographics, it isn’t particularly called for. For example, Malaysia has a large number of guest workers, and the same is true of Thailand (albeit with the important caveat that some of the latter are in Thailand illegally) but it is in Hong Kong where these questions loom largest. Immigration from mainland China developed Hong Kong in the first place, and will continue to be a driver. There’s already a large inflow of skilled professionals from China, but inflows of lower skilled workers are more tightly controlled. The critical issue is whether policy, and property prices, will allow this immigration to happen on a sufficient scale.

Raising birth rates: Although it takes longer to have an impact on worker numbers, the other key lever here is the potential to lift birth rates once more.

To be clear, bigger isn’t necessarily better. Accepting young, highly skilled migrants, a longstanding policy in Australia, has the potential to boost all three of the building blocks of economic potential at the same time: population, participation, and productivity.

So a key test of Asia’s political systems looms: As countries grapple with the effects of ageing, nations able to politically sustain solid levels of net immigration, especially of higher skilled workers, will grow faster than those that can’t. And regardless of whether working age populations are still rising, the same will be true of nations that welcome women workers as openly as they do men.

Girl power: What India can gain from its women

India’s potential workforce will rise by 115 million people over the next decade—and account for more than half of the 225 million strong workforce increase expected across Asia as a whole.

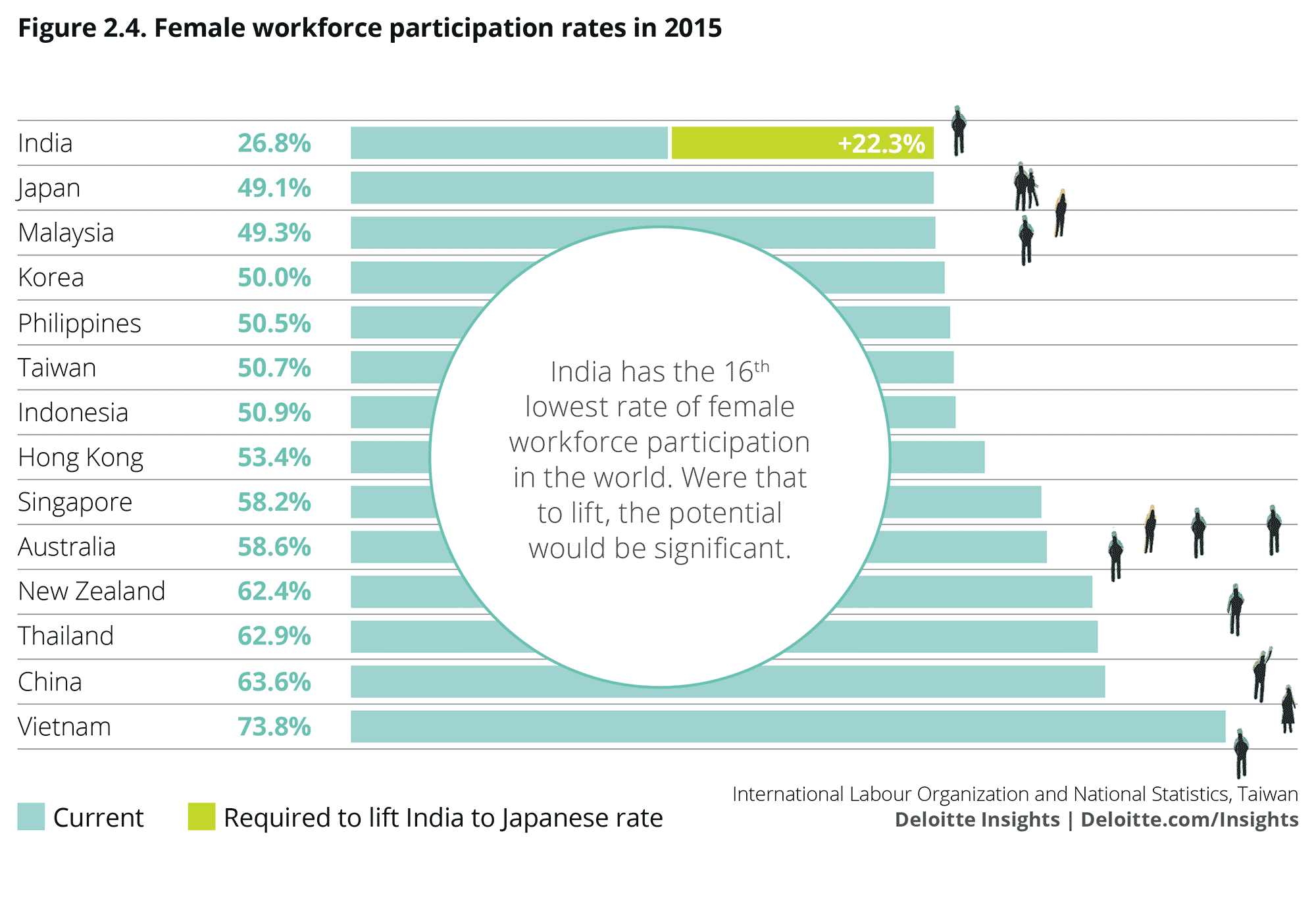

But just how well will ”potential” translate into ”actual”? India has the 16thlowest rate of female workforce participation in the world. Were that to lift, it would turbocharge the demographically driven boost to India’s economy over coming years.

Compare two cases—one where India’s female workforce participation rates remain at 27 percent, and another where it gradually rises to 49 percent (equal to Japan’s current position) by the 2030s. This may seem like a huge leap, but it would merely lift India to the second lowest of the countries shown in figure 2.4.

Please click on the graph to enlarge.

Such a change would nearly double the number of women working in the paid economy, with the extra workers lifting the overall size of the workforce by more than 20 percent above its expected level.

And, even after noting that women tend to receive lower wages than men, this would boost the overall size of the Indian economy by around one sixth, or the equivalent of close to US$2 trillion a year in terms of today’s purchasing power.6

So there is a huge incentive to act; yet getting there won’t be easy. Japan, with female participation rates still below 50 percent, shows that even after a long period of grappling with the need to boost female participation, progress can be slow.

And there’s more than just who—there’s how and where

Different economies will see other factors impact the challenges they might face. The previous article, Ageing Tigers, hidden dragons, noted that both growth in population and a change in the type of lifestyle these populations might wish to enjoy will put increasing pressure on the environment, both in terms of the demands on food and water and the pollution that might result. These challenges can also be driven by choices made in the past and that are still affecting the environment today.

The long-running impacts of urbanisation continue to be felt across Asia. While the rise in China’s population has been important to its success, the internal movement of people from rural regions to the cities has been just as important. Official estimates have put the level of internal migrants at over 10 percent of the country’s population7—150 million—with other estimates suggesting that the true figure is more than twice that.8

Urbanisation leads to differing issues across the economies of Asia—both positive and negative. In the faster-growing areas of Indonesia and the Philippines, the huge construction requirements the trend brings are clearly a massive business opportunity, but where development is too slow, problems around housing availability can be dangerous for social cohesion.

Gaps between the richer urban areas and the impoverished countryside can also exacerbate the risks of the ”middle-income trap”—where a period of strong economic development stalls.

Demographics may add further to the risks, with declining workforce levels not only leading to increasing pressure on wages and limiting international competitiveness, but also increasing demands on public expenditure on the elderly through pensions or health care.

Millennials to the rescue?

This report sets out the challenges arising from the great tides of demography. Yet, demography isn’t manifest destiny. Weakness in growth potential as a result of an ageing population can be offset if the rising generation can bring sufficient productivity benefits.

That, for example, is the test for China. Its population is ageing and its potential workforce is already beginning to shrink. The good news is that it is likely that the younger workers swelling the ranks of the employed over the next decade will be able to fight off some of those demographic difficulties.

The first edition of Voice of Asia9 noted that the young people of Asia were revolutionising marketplaces: “A new and optimistic generation is taking its place in driving the direction of their economies: One that is technologically savvy, comfortable with the borderless consumerism of the global middle class, and yet imbued with the consumption-smoothing instincts of its parents and grandparents. These new consumers are exactly what Asia and the world need right now. They’re inherently optimistic and incredibly open to innovation and new ideas.”

That’s a very Asian story, with this region’s youth front and centre in the global roll call of optimism. Our own research on Millennials10 found a chasm between the developing world and the rich world when it comes to the outlook of the younger generation. Millennials in emerging markets expect to be both financially (71 percent) and emotionally (62 percent) better off than their parents, whereas in the developed world only 36 percent of Millennials predict they will be financially better off than their parents, and a bare 31 percent say that they’ll be happier.

And times are changing fast. There is a new class of consumers, as we are going from “Millennials” to “Minimals.”11 They carry some traits of the Millennials, but aim to declutter their lifestyle by minimising asset ownership while still getting the services they desire. In a minimalist economy, ownership of assets is lowered as services are preferred over products and Minimals instead invest in health, well-being, and productivity. The sharing economy is perhaps a source and a product of the advent of the Minimals.

Yet, it is the behaviour of the young as producers which may prove even more revolutionary than their behaviour as consumers. In both India and China, the next generation to join the workforce will be rather better educated than the average of the current workforce.

In turn, this may enable these younger workers to unlock the power of new digital technologies with increased ”productivity potential” covered in edition two of Voice of Asia.12

These trends in lifestyle, whether workforce participation or productivity, will be just as important as demographics to overall economic trends in the decades to come. Long-term projections for economic growth across the next 40 years13 show the Indian and Indonesian economies leading the way in terms of speed, growing at close to 5 percent per year.

And while China’s growth might be hampered by its more negative demographics, the 3.3 percent average growth rate forecast would mean one economy would still account for more than a quarter of all economic growth around the world across this period.

Add India and Indonesia, and the three biggest Asian economies will account for more than half the world’s economic expansion between now and the middle of the century.

So some things might be set to change, but Asia’s role as the world’s business powerhouse is not one of them.

Endnotes.

- The figure matches figure 1.4 in the first article in this edition, but covers the likes of Europe and North America as well.

- The National Bureau of Economic Research, Population aging and economic growth, 2016.

- International Monetary Fund, Euro area politics, July 2016, http://www.imf.org/external/pubs

- /ft/scr/2016/cr16220.pdf

- Wall Street Journal, “Demographic 2050 destiny”

- Most results are from the International Labour Organization (ILO), with the exception of Taiwan, which is sourced from National Statistics, Republic of China (Taiwan)

- Based on 2011 PPP measures. As the purchasing power of money goes further in India, the addition to India’s economy is smaller than that at market prices, but it is the US$ 2 trillion figure that provides the more accurate assessment of the impact on world well-being. Note that this result is consistent with the analysis undertaken by the the ILO, Reducing gender gaps would significantly benefit women, society and the economy and How much would the economy grow by closing the gender gap?

- Cai, Fang, Yang Du, and Dewen Wang (eds.), Report on China’s population and labour, 2011

- Kang Wing Chan and Peter Bellwood (eds.), China, internal migration, 2011,

- Deloitte University Press, “A rich tapestry of insights,” Voice of Asia

- Deloitte, The Millennial survey View in article

- Minimals: A cohort of people belonging to the younger demographic within the Millennials whose expenditure patterns are distinctly geared towards acquiring services rather than assets

- Deloitte University Press, “Asia winning the race on innovation, growth, and connectivity—powered by digital,” Voice of Asia

- OECD, “GDP long-term forecast”

See also link to the original source here.

A Chinese law firm and a member of the Deloitte Legal global network, we are well positioned to provide integrated solutions to address your business and legal issues within and outside China. "Deloitte Legal" means the global network of legal practices which are affiliated with Deloitte Touche Tohmatsu Limited member firms. Shanghai Qin Li Law Firm, a licensed Chinese law firm, is the China member of that global network.

For further information, please contact:

Clare Lu, Partner, Qin Li Law Firm, a Chinese law firm and a member of the Deloitte Legal global network.

cllu@deloittelegal.com.cn

Mark Schroeder, Qin Li Law Firm, a Chinese law firm and a member of the Deloitte Legal global network.

marschroeder@deloittelegal.com.cn