31 March, 2020

The Belt and Road Initiative (BRI) is a historic marshalling of capital and a remarkable geopolitical foray into establishing and strengthening multinational trade corridors. With over US $440 billion of funding provided by Chinese financial institutions for BRI projects so far, it's an enterprise unlike anything seen on this scale for decades and holds tremendous opportunities for business. The BRI continues to evolve and expand with more than 130 countries now reported to have signed BRI agreements, far beyond the traditional Silk Road routes.

How will COVID-19 impact the nature, pace and scope of BRI activity in the near and longer-term future? New research from Silk Road Associates shows that we can expect the quality of BRI to improve owing to the greater participation of the private sector and foreign companies, as well as BRI’s tighter alignment with the global supply chain.

COVID-19 has already had significant impact on the global economy, affecting manufacturing, supply chain and the movement of people and goods. As China mobilizes resources to manage the containment of the virus, it also has to balance challenges to Chinese liquidity and the general economic downturn.

As ripple effects of the Coronavirus are being felt across the globe, the nature, pace and scope of BRI activity will also be affected, both in the near and longer-term future. Despite challenges to manufacturing and supply chain activity, the pace of digital BRI activity has ramped up as have investor interest in Chinese tech companies and in the general healthcare industry.

This paper, which includes research from Silk Road Associates (SRA) and insights from Baker McKenzie, provides an overview of three key areas in which COVID-19 alters the flow of BRI activity. It also offers an updated outlook regarding several BRI scenarios previously produced by SRA and Baker McKenzie, showing that the quality of BRI activity should in fact continue to improve, owing to greater participation of the private sector and foreign companies, as well as BRI’s tighter alignment with global supply chains.

“The COVID-19 epidemic definitely has a dampening effect on BRI activities as Chinese companies focus their resources and efforts on dealing with the various types of impact caused by such epidemic. However, this effect will likely be relatively short term and we are already seeing the resumption of BRI activities by our Chinese clients. It is also heartening to see foreign sellers and partners adjusting their deal timetables to make allowances for the impact caused by this epidemic.”

Bee Chun Boo M&A Partner, Beijing, Baker McKenzie

Fundamental Change in Global Supply Chains

Since 2018, Chinese companies have refocused their efforts on the larger markets of Southeast Asia where supply chain linkages with China are strong and investment returns are more predictable. COVID-19 will only supercharge the ongoing momentum of Chinese private manufacturers investing in Southeast Asia or consider their options.

A growing number of Chinese manufacturers, alongside their mainly North Asian partners, will seek to build capacity across Southeast Asia and hedge against the rising risks of supply chain disruption. In turn, Chinese infrastructure investments in Southeast Asia will benefit from these flows. Additionally, Chinese state companies are focused on investments in ports, power, and industrial parks across Southeast Asia, especially where these projects are aligned with Chinese investment into manufacturing and also support the development of Chinese commercial ecosystems in the region.

“Southeast Asia will likely be the focus for Chinese manufacturers, especially Vietnam, which has captured the overwhelming share of factory relocations. Other areas of potential for Chinese manufacturing activity will be options in South Asia and Mexico.”

Ben Simpfendorfer – Founder and CEO, Silk Road Associates

Expedited Digital BRI

Opportunities abound for full digital value-chain for digital BRI activity, from ICT companies to e-commerce platforms, including firms which are well established throughout the BRI geography such as Huawei, Alibaba, and Tencent.

It will be natural for Chinese tech companies such as Alibaba’s DingTalk, Tencent’s WeChat Work and Huawei’s WeLink to bid for market share outside of China, especially in the BRI region. China’s MedTech sector may similarly find opportunities abroad. Online doctor consultation platforms have seen consultations soar in the past few months (Alibaba Health, Ping An Good Doctor) and similar technologies may work abroad if staffed by locals, given health sector shortfalls in many BRI countries.

Simpfendorfer adds that “China’s success in using AI and other technologies to identify and monitor virus carriers may also have application across the BRI, especially in those countries, such as India and Thailand, which are currently developing smart cities and where China’s technology companies are already heavily committed.”

“Digital application of technology and big data have been widely used in China to help fight and contain the virus and mitigate disruption to business continuity in a rather effective way. Hence, we expect digital BRI activity will attract more interest from local companies in those jurisdictions in having deeper and broader scope of collaboration with Chinese tech companies around their proven technologies and business implementation models.

The increase of digital BRI activity will also promote and contribute to more frequent and increase volume of cross-border business data flows and lead to collaboration between Chinese government and the governments of other jurisdictions involved in BRI in terms of legislation concerning cross-border data transfers.”

Zhenyu Ruan – Senior Counsel, FenXun Partners

Rise of Private Sector Involvement

Chinese state banks will face greater capital constraints over the coming 12 months and NPLs are likely to rise at home, owing to COVID-19 related financial weakness even as investments into the domestic health sector or other related infrastructure increase.

Chinese private financial sectors will need to fight against weakening domestic conditions to play an even greater role if Chinese state banks reduce funding. The private sector will likely focus on the most commercially profitable supply chain related investments, especially those related to industrial or mixed-use commercial projects that benefit from the relocation of production away from China to other low-cost destinations, as well as sales to the domestic market and BRI countries.

“In response to COVID-19, we should expect to see the Chinese private sector capture the opportunity presented by the inevitable diversification of supply chain operations and production in China and its impact on domestic production and export. No sector will be immune but we anticipate industrial manufacturing will be the most challenged and conversely, present the greatest opportunity for investment and growth.”

Martin David – Asia Pacific Head of Projects, Singapore

Greater Opportunities for International Collaboration

The US-China trade war and COVID-19 only further incentivize China to adopt a more collaborative model towards BRI. BRI projects will increasingly focus on profitable supply chain related opportunities in Southeast Asia where the private sector and private capital play a greater role. Even as COVID-19 has put a spotlight on the importance of supply chain diversification, the virus may similarly nudge BRI governments to think about their overdependence on a single country, especially should travel restrictions become a routine exercise each winter.

Conclusion

Whatever the lasting impact of COVID-19 on the global economy, BRI will remain a priority for China. What remains important will be the government’s short-term and long-term response to the virus, shortfalls in China’s health sector, and the economic fallout for the country’s financially challenged SME sector. This will likely divert official attention and resources away from BRI over the next 12 months and potentially longer.

The reduced flow of Chinese capital, as well as the economic fallout for the country’s financially challenged SME sector, may bring about a less enthusiastic attitude towards the BRI over the following 12 to 24 months and China’s priorities shift to delivering results at home, rather than abroad. This may mean reduced investments into BRI’s smaller, less critical markets where the opportunities to connect such investments to the global supply are limited. Central Asia, Sub-Saharan Africa, and Eastern Europe will accordingly see a short-term dip in BRI related activity, relative to Southeast Asia.

However, the outlook is far from bleak. China will seek to share its valuable experience of battling COVID-19 with other BRI countries. One key area of potential is in projects focused on strengthening the health systems of low-income countries, even if focused on soft processes rather than hard infrastructure. This would be a potential area where China is likely to publicise its efforts as being a part of the BRI.

Beyond the short-term, changes to global supply chains bring new opportunities for diversification through joint activity with others in both in North and Southeast Asia. There is also potential for accelerated digital BRI activity in relation to Chinese tech companies and private players may now become more active in BRI.

Discover more BRI resources on sustainability, funding, risk mitigation and more, including an infographic produced in partnership with Silk Road Associates on five key BRI scenarios. Visit our BRI and Beyond Hub.

BRI Beyond 2020: Fresh Insights

The Economist Corporate Network, supported by Baker McKenzie, has produced two reports on BRI, exploring how China is taking steps to reboot its approach to BRI projects with the goal to increase international participation and encouraging a multilateral approach that is more inclusive, sustainable and transparent.

|

|

| >> Download ENGLISH version | >> Download ENGLISH version |

| >> Download CHINESE version | >> Download CHINESE version |

Unique Insights on Essential BRI Trends

See what our partners have to say and gain insights on crucial BRI challenges and opportunities relating to risk management, sustainability, funding and project management.

|

|

| >> Download report | >> Download report |

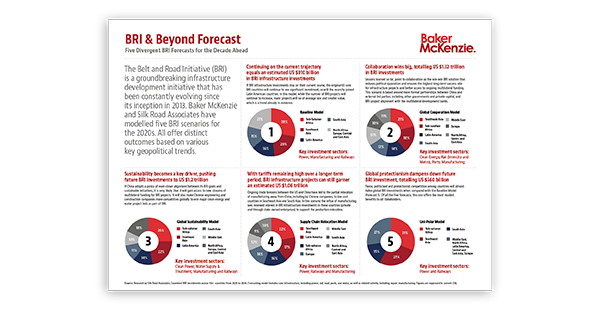

BRI & Beyond Forecast

Assessing five vastly different scenarios of possible development for BRI investments in the coming decade.

Please click here to download.

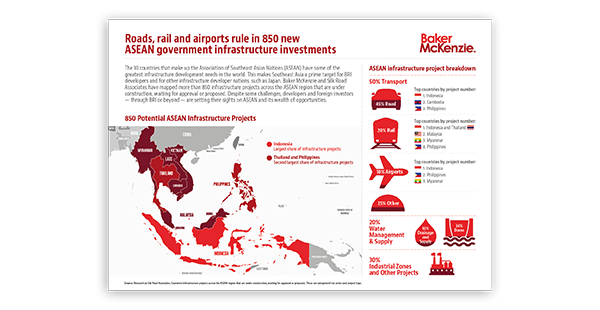

BRI Investment Hotspots

Exploring the countries and regions primed for BRI investment based on our forecast.

Please click here to download.

For further information, please contact:

Milton W. M. Cheng, Partner, Baker & McKenzie

milton.cheng@bakermckenzie.com