.jpg)

2 May, 2019

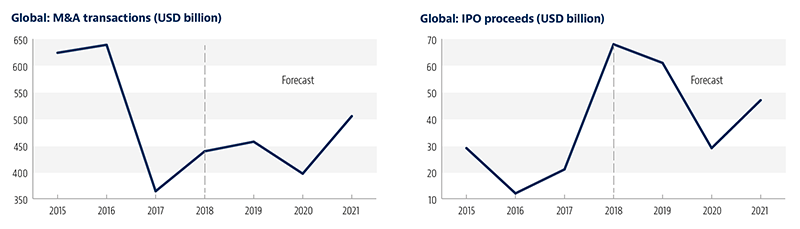

Mergers and Acquisitions (M&A) activity in tech and telecoms rose to USD 439 billion in 2018 as transformations within the sector continued and the emergence of disruptive cloud, mobile, social and big data analytics technologies drove deal making. The sector had an exciting and strong year for M&A, up 21% from 2017. Megadeals have dominated the headlines.

According to our Global Transactions Forecast, issued with Oxford Economics, big-ticket transactions set for completion in 2019, and favourable market trends are expected to increase M&A activity, with deal values predicted to increase a further 4% to USD 457 billion.

Michael DeFranco, Global M&A Chair, said: "Despite the challenges facing the sector, businesses in all industries are increasingly looking to technology to change the way they do business and propel them in their markets. As the convergence of media and technology, direct-to-consumer capabilities, the cross-sector acquisition of technology, and the expanding demand for data and AI continue, deal making in tech and telecoms will remain buoyant in 2019."

IPO value in tech and telecoms rose to USD 68 billion in 2018, compared to USD 21 billion in 2017, boosted by large listings as well as activities relating to spin-offs from the big tech players. Chinese tech start-ups also continued to look at the US for better fundraising options.

A growing market

Changing business models, expansion of the giant tech players, new and more nimble competition and emerging technologies, such as AI and 5G platforms, are driving activities. With all the signs pointing to a market that will continue to grow, success in the sector will likely involve significant convergence of M&A and transactional activities.

Some transactions have been driven by traditional TMT M&A trends, such as the need for scale and competition for best-in-class technology, talent and content; however activity in new tech is booming, with a wider range of buyers aiming to innovate through acquisition and as acquirers seek global expansion.

For technology, AI is going to be hugely active as machine learning and cloud-based services drive demand. Software companies will also continue to seek acquisitions that will allow them to sell suite solutions across multiple functional verticals. For telecoms, 5G networks will play a crucial role and we have already seen forward looking alliances in media.

Mobility and e-commerce

M&A partner Roel Meers said: "The consumer and e-commerce sector will also see big increases in M&A activity in 2019 compared to 2018, particularly as economic stability directly impacts consumer spending ability."

Elsewhere, mobility and e-commerce are continuing to drive activity. In the automotive sector, triggered by the increased adoption of autonomous technology in vehicles, there has been

significant investment with key partners getting together to co-invest to bring profitability to the sector. In the consumer goods and retail sector, will also expect to see big increases in M&A activity over the next year with the continued disruption of traditional retail models driving further acquisitions to build ecommerce and omnichannel capabilities.

Consolidation and convergence going forward will continue to be the name of the game as electronic communications and technology set the scene in the transportation and e-commerce ecosystems.

Regulatory and data privacy challenges

Despite the dynamic and exciting market developments, growth in tech and telecoms has been somewhat more muted than anticipated, reflecting an increase in regulatory scrutiny, particularly regarding major deals in the microchip sector that have been looked at by regulators, adding an overlay of market concern around significant market power.

In case of a change of control (in the broadest sense), governmental scrutiny to protect "strategic assets" – such as those in the telecoms, energy, transportation and defence industries – might affect technology and telecoms transactions, especially along certain trajectories such as Chinese investment into the US. The extended powers of State bodies could therefore affect the transactional landscape. And this not only in the United States (especially with the recent legislative developments around CFIUS’ role and jurisdictions), but also in the EU with increased focus on Chinese investments.

Data privacy is also expected to have impact on M&A activity in the next 12 months, particularly with the introduction of the European Union’s General Data Protection Regulation and the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) trade agreement, and data increasingly seen as a key asset.

A global outlook

The US and Europe will play major roles in deal making in 2019, with China more than likely at the forefront of activity, especially as it is already looking at new and sophisticated technologies such as 6G. In Asia, the vivacious atmosphere and environment create excellent conditions for transactional opportunities. Africa will also be a region for significant potential in the tech space.

M&A partner Roberto Grane said: "Transactions during the last year in Argentina have been focused on infrastructure investment, including towers and comparable structures that can increase the reach of signals and services. 5G will require new investments and all developments in technology and telecoms rely on infrastructure availability, which in many jurisdictions is of a very low quality. We believe this trend will increase during 2019."

With all the signs pointing to a market that will grow rapidly in 2019, the cutting edge and exponential growth nature of technology will mean that the sector will continue to be on a high, enjoying a period of substantial activity that would result in a major uptick in the number of well-structured deals being completed, with the sector concurrently exhibiting no obvious signs of being curtailed.

For further information, please contact:

Raffaele Giarda, Partner, Baker & McKenzie

raffaele.giarda@bakermckenzie.com