Introduction

As Central Asia continues to develop towards sustainable energy solutions, the significance of well-drafted Power Purchase Agreements cannot be overstated. Unicase Senior Partner Saniya Perzadayeva has presented the Financing Renewable Energy Projects and Bankability of PPAs in the context of the Central Asia Green Energy & Hydrogen 2024 forum in Tashkent and Energy Week Central Asia and Caucasus in Astana.

Power Purchase Agreement

A PPA is a long-term contract established between an electricity producer and a buyer, typically a utility, government entity, or corporation.

The Required Conditions to make PPA effective:

- Comprehensible text (concept, terminology);

- Fair allocation of risks between the Parties;

- Predictability of key elements (fees, the liability of the parties, etc.);

- Procedures and instruments to address problems (non-performance of obligations, compensations, force-majeure, etc.)

A bankable PPA is a long-term contract structured to meet the financial requirements of lenders and investors, ensuring reliable revenue and minimising risk for energy projects.

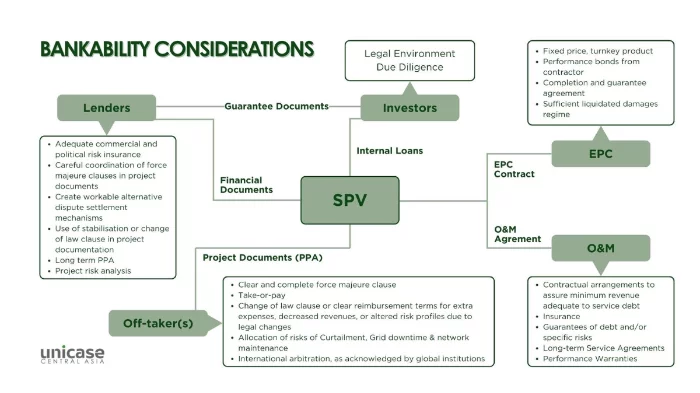

The following scheme outlines Bankability Considerations

Key Terms and Conditions of Bankable PPA, International Practice

Firstly, a clear set of definitions is critical for a bankable PPA. This guarantees that all parties have a mutual understanding of the terminology used throughout the agreement.

The term of the agreement typically ranges from 15 to 25 years. This duration provides stability for the energy buyer and the power generator, allowing for long-term planning and investment.

A fundamental aspect of many PPAs is the Take-or-Pay provision, which guarantees the purchase of all generated electricity. Take-or-pay is a common contract where the supplier undertakes to deliver the goods in volume under the contract, and the buyer undertakes to pay a certain part of the volume, regardless of the actual purchase. While such rules are prevalent in Uzbekistan, it is essential to note that Kazakhstan currently lacks similar experience in this area.

In addition to pricing mechanisms, a fixed tariff and considerations for foreign exchange fluctuations must be established to protect against market volatility.

The agreement should also detail the regulation of dispatching, balancing, and forecasting to secure efficient energy management and grid stability.

An implementation schedule with clear milestones, including the financial closing period and associated penalties for delays, is vital for maintaining momentum in project development. This structured approach provides accountability and timely progress throughout the project lifecycle.

Furthermore, a precise definition of the Commercial Operation Date and a defined procedure for achieving is necessary. A trial run or COD test must also be conducted, with specific minimum performance criteria that need to be met.

Based on the international practice, provisions for curtailment, grid downtime, and network maintenance should be included in a PPA to address potential service disruptions. It is essential to account for reductions in power delivery due to project outages by the Seller or unscheduled grid downtime caused by the grid operator, who may or may not be the same party as the buyer.

The agreement should also outline assignment and step-in rights, allowing for flexibility in the management of the agreement.

The PPA should contain clear and detailed force majeure provisions, which will excuse a party’s performance for reasons beyond its reasonable control and will extend the milestone deadline. It is important to draft the force majeure clause properly in case of choosing common law countries as governing laws since force majeure has no real meaning under the common law.

In the event of non-compliance or other issues, the agreement should specify termination clauses and associated termination payments to provide a clear exit strategy. The PPA should list early termination events and a clear methodology for determining termination payments. Termination events generally include (1) insolvency events or similar; (2) default in the performance of obligations under the PPA when not cured or remedied within the specified period, including failure to meet conditions precedent, failure to meet licensing or permitting requirements, failure to make payments due, and Reaching the limit of liability.

Provisions related to change of law and qualified changes in law should be included to address any legal adjustments that may arise during the contract term. The change in law clause protects the developer against changes to applicable laws and regulations or new laws introduced after the PPA is executed, which may have a financial impact on the project.

Lastly, it is mandatory to incorporate international arbitration mechanisms. It is important to note, however, that many international financial institutions do not recognise the AIFC International Arbitration Centre (IAC) as an international arbitration. However, we should note that the IAC may be considered a good option in terms of the costs compared to the costs of other institutions. The IAC also offers parties maximum choice and flexibility in choosing the rules and procedures. For example, IAC may administer their arbitration according to UNCITRAL Arbitration Rules or ad hoc arbitration rules as well as to provide other forms of alternative dispute resolution.

Integrating these terms and conditions into a PPA will provide a strong foundation for an effective and successful energy partnership. Additionally, off-taker payment support mechanisms should be established to enhance financial security for the energy generator.

Bankability issues in Kazakhstan:

In Kazakhstan, a PPA with the single off-taker is executed based on the approved template. Such templates, as well as the legislation on the RE, lack certain rights of investors that result in a low bankability level of the project.

One significant area of concern is the change of law clause. A PPA lacking a well-defined change of law clause or clear reimbursement terms can lead to complications: Kazakhstan’s model PPA lacks a change of law clause. There is no specification of who will reimburse the Seller if legal changes lead to the Seller incurring extra expenses, decreasing revenues, altering the Project’s risk profile, or diminishing shareholders’ economic returns.

Furthermore, there is no transparent calculation method for reimbursement. Without these provisions, parties might encounter surprise costs, lower revenues, or shifts in risk because of relevant changes.

Another critical component is the force majeure clause, which can often be vague and incomplete, leaving parties uncertain about their rights and obligations in unforeseen circumstances.

A take-or-pay clause entails an arrangement wherein the purchaser commits to either accepting the generated power or compensating for it if it goes unused. According to the Kazakhstani RE Law, the single buyer is obliged to buy electricity produced and supplied to renewable energy-producing organisations. However, the legislation does not oblige energy transmission organisations to take into the grid and transfer all electricity produced and delivered from RES. In this regard, there is a risk that the developer may be provided with a connection point, but the power transmission company refuses the acceptance and transfer of the entire amount of electricity produced for various reasons, including objective ones. Both the RE Law and the PPA should ensure payment to the developer for all the electricity generated (the Take-or-Pay principle).

Issues surrounding curtailment, grid downtime, and network maintenance also warrant attention. The risks associated with these factors are not allocated in the Kazakhstan Model PPA. The risk is on the off-taker rather than a project company. Regardless of whether the system operator dispatches the power plant or merely “takes” the electricity that could be produced when the power plant is available to generate, the off-taker is still obligated to pay. The lack of explicit risk allocation can lead to disputes and uncertainty regarding responsibilities.

Lastly, international arbitration is important for resolving potential disputes. Many international financial institutions do not recognise the AIC as an international arbitration as of yet.

Potential strategies to address the bankability challenges of PPAs

Kazakhstan has the potential to strengthen its investment landscape significantly through mitigation initiatives. A fundamental step in attracting foreign investment is the improvement of legislation. Streamlined and transparent regulatory frameworks are essential for creating a business-friendly environment. Reducing bureaucratic barriers and enhancing the transparency of legal procedures in Kazakhstan can foster increased investor confidence, thereby creating a foundation for sustained economic growth and development.

What should Kazakhstan do to maintain its investment prospects?

Another tool to mitigate the drawbacks of model PPAs could be concluding Investment Agreements (IAs) and/or Intergovernmental Agreements (IGAs). An IA is an agreement for executing an investment project based on a decision made by the government. An IA requires investments amounting to at least USD 58 million.

An intergovernmental agreement (IGA) is made between two or more governments. IA agreements may be concluded within the framework of IGA.

A ratified IGA can offer specific exceptions from local laws, making projects more appealing and financially viable. This flexibility is vital for addressing the unique needs of foreign investors and ensuring that projects can proceed without undue regulatory burden.

Opportunities and Limitations of IGAs in Kazakhstan

IGAs play a crucial role in facilitating foreign investment in Kazakhstan. While they offer several advantages, they also present certain challenges that investors must navigate.

Positive Factors and Opportunities

One of the most significant advantages of ratified IGAs is their legal precedence over national legislation, as stipulated in Article 6.2 of Kazakhstan’s Law on Normative Acts. This provision allows IGAs to introduce terms that may diverge from existing national laws.

Some of key opportunities include:

- Power Purchase Agreements Without Auction: IGAs can permit the signing of PPAs without a competitive bidding process, streamlining project initiation.

- Currency Arrangements: Investors may set the USD exchange rate or establish tariffs in foreign currencies, providing greater financial predictability.

- Land Acquisition: IGAs can facilitate land acquisition outside the auction process, simplifying project selection.

- Regulatory Framework: Projects can be regulated under English law or other legal systems, which may offer more favourable dispute resolution mechanisms.

- Customisation of Contracts: Investors can bypass standard forms, allowing for tailored contractual agreements that better suit their needs.

- International Arbitration: Dispute resolution can be allocated to recognised international arbitration centres such as London or Hong Kong, ensuring a neutral ground for conflict resolution.

- Compensation Provisions: There may be stipulations for state compensation upon termination of project agreements, offering additional financial security.

- Deemed Energy and Take or Pay Clauses: These provisions can enhance project viability by providing a guaranteed revenue stream.

- Legislative Stability: The stability of legislation surrounding IGAs can provide a more predictable investment environment.

Limitations and Negative Factors

Despite the advantages, there are notable limitations to consider:

- Parliament Ratification Required: For an IGA to be effective, it must undergo ratification by the Parliament of Kazakhstan, which can be a significant hurdle.

- Case-by-Case Evaluation: Each IGA is assessed individually, meaning outcomes can vary significantly based on specific project circumstances and stakeholder support.

- Risk of Non-Ratification: Parliament is not guaranteed to ratify the IGA even after extensive negotiations and incurred preparation expenses. The support and networking capabilities of Kazakhstani developers can greatly influence this process.

- Potential Legislative Amendments: Implementing the terms of an IGA may require changes to existing legislation, which can complicate and prolong the process.

- Lengthy Ratification Timeline: The ratification process can take one to two years, adding to the uncertainty and time investment needed for project initiation.

Mitigating strategies

In Kazakhstan’s evolving investment landscape, it is critically important to implement effective mitigation strategies for attracting foreign capital, particularly in the energy sector.

One essential element is the inclusion of arbitration clauses in both IAs and IGAs. These clauses are critical for resolving disputes, giving investors confidence that their interests will be protected and conflicts can be resolved fairly and efficiently.

Another significant advantage of IAs is the potential to guarantee the stability of legislation throughout the project’s duration. Investors prioritise a consistent regulatory environment, which permits them to make informed decisions and long-term commitments. By securing legislative stability, Kazakhstan amplifies its attractiveness as a destination for investment.

Setting up bankable PPAs is also important. A well-structured PPA provides financial security and a predictable revenue stream, making investments in renewable energy more appealing. Robust and favourable agreements can significantly contribute to drawing capital into the sector.

Furthermore, the protective measures included in IGAs are of utmost importance. These safeguards investors from potential risks and uncertainties, creating a more secure investment climate that encourages foreign participation.

Lastly, addressing the concept of deemed energy and implementing provisions for take-or-pay curtailment is necessary for establishing that renewable energy producers are fairly compensated for their contributions, even during curtailment situations. This assurance provides a safety net for investors and strengthens the overall feasibility of energy projects in Kazakhstan.

Unicase is a leading Central Asian law firm operating locally and internationally, with a strong presence in Kazakhstan, Uzbekistan, Kyrgyz Republic, Tajikistan, and Turkmenistan. Unicase has one of the strongest Expert Teams, well known for regulatory and law drafting capabilities, who, alongside a strong transactional background and expertise, have allowed the firm to win major development projects and continue to be the first-choice advisers for legislation development issues.