Background

Since 2025, gold has experienced a historic bull market, with international gold prices rising by more than 70% at one point. According to the Gold Demand Trends: Q4 and Full Year 2025 released by the World Gold Council on January 29, 2026, the value of global gold demand surged to an unprecedented USD 555 billion. Against a backdrop of global geopolitical and microeconomic uncertainty, an increasing number of investors are turning their attention to gold, a long-term asset for risk hedging and value preservation.

Following this trend, Hong Kong Chief Executive John Lee Ka-chiu, in his speech at the 19th Asian Financial Forum, stated that Hong Kong is committed to building an international gold trading center. The goal is to increase gold vaulting capacity to over 2,000 tons within three years and establish a central clearing system, positioning Hong Kong as a regional gold reserve hub. In a recent media interview, Lee mentioned that Hong Kong’s gold trading market currently operates on a membership basis, which limits participation in investment and trading. In the future, gold trading would be as convenient as stock trading, allowing global investors to participate, supported by an efficient and trustworthy clearing and settlement system.

The enthusiasm of offshore investors for gold, coupled with the high barriers to entry in traditional gold markets, has created immense possibilities for gold tokenization. Compared to holding physical gold and investing on other gold-related financial products, tokenized gold offers lower entry threshold and enhanced liquidity by leveraging 24/7 blockchain-based infrastructure, providing investors with a more convenient and efficient investment channel. In addition, tokenized gold ensures investors’ ownership of the underlying physical gold through various measures such as independent third-party audits and redemption for physical delivery. Consequently, gold tokenization is poised to become the new favorite in real-world asset (RWA) tokenization in 2026.

This article provides an in-depth analysis of the advantages of tokenized gold (RWA tokenization) over other gold products, as well as the basic structure and key considerations for gold tokenization projects in Hong Kong.

1. Definition of Gold Tokens

Gold-backed tokens typically refer to digital tokens issued and recorded on a distributed ledger (including blockchain-based DLT) that represent legal title, beneficial interests, or other economic rights in respect of physical gold held in custody by a custodian. Each token is typically backed by (and pegged to) a specific weight of physical gold, such as one gram or one troy ounce.

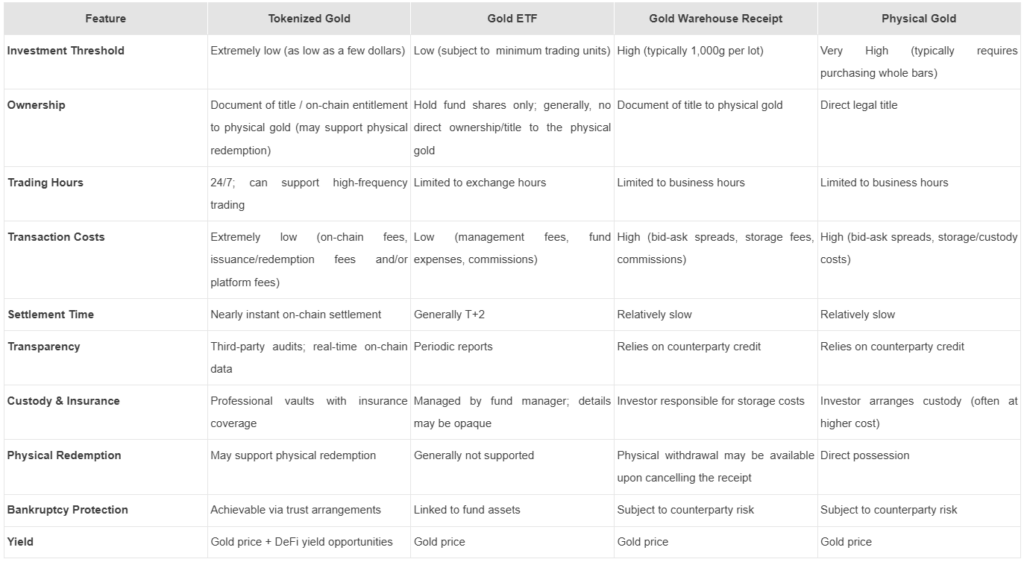

2. Advantages of Gold Tokenization

Gold, one of the oldest stores of value in human history, has long been regarded as a safe-haven asset and an inflation hedge. However, its physical characteristics – being bulky and heavy, difficult to divide, expensive to transport, and subject to slower delivery/settlement – have historically constrained its accessibility and liquidity as an investment product. Traditional products like gold warehouse receipts, gold futures contracts, and gold ETFs address certain pain points around storage, transportation and delivery but they still rely on centralized clearing and settlement infrastructure, which can result in settlement delays and restricted trading hours. These products also involve multiple intermediaries, resulting in high transaction costs.

Gold tokenization seeks to address these frictions by issuing on-chain digital tokens backed by a specified weight of gold, thereby enabling fractionalization of ownership/economic interests in bullion and lowering the investment threshold. In addition, the 24/7 ledgering and settlement functionality of blockchain-based infrastructure can reduce friction costs and support more continuous (including higher-frequency) trading. Tokenized gold projects can enhance transparency and verifiability through measures such as independent third-party audits and on-chain recording (or real-time updating) of the quantity of underlying gold, helping investors to evidence their rights/entitlements in the underlying asset. Some tokenized gold projects also offer physical redemption (i.e. redemption for physical delivery), providing additional convenience for investors who ultimately wish to take delivery of physical gold.

Compared with other more price-volatile virtual assets, tokenized gold may offer investors a relatively more stable source of value.

We summarize the key advantages of tokenized gold in the table below:

Information Source:(1) https://www.osl.com/hk/bits/article/future-of-digital-gold, (2) https://www.hashkey.com/zh-TW/blog/insights/2026-gold-tokenization-investment-guide

Comparison Table: Tokenized Gold vs. Traditional Gold Products

3. Key Elements of Hong Kong Gold Tokenization Projects

Building a compliant gold tokenization project involves collaboration among multiple parties. A reasonable project structure and implementation plan should be designed with regard to investors’ preferences as well as the applicable laws and regulations of the jurisdictions involved.

3.1 Involved Parties

(1) Token Issuer

The issuer is a crucial component of the entire gold tokenization project architecture. The jurisdiction in which the issuer is established and the legal form of the issuer must be determined by reference to the legal nature of the token as well as the securities-related laws and regulations applicable to the jurisdictions where the token is offered, marketed and distributed, ensuring that the issuer can offer and sell the tokens in compliance with the applicable requirements in investors’ respective jurisdictions. The token issuer is not necessarily required to directly hold the underlying gold; it may also hold interests in the underlying gold through contractual arrangements. If the gold tokenization project allows investors to redeem physical gold, the issuer should also consider whether it needs to obtain a precious metal dealer license or registration in the relevant jurisdiction(s).

(2) Physical Gold Holder

Depending on the location of the physical gold and the relevant account-opening requirements of the gold dealer and/or gold custodian, the underlying gold in the gold tokenization project may be held by an appropriate designated entity. This is to ensure that token investors can directly benefit from/enforce their entitlements to the underlying gold and that the underlying gold is legally segregated from the bankruptcy of the token issuer or the holder of the physical gold.

(3) Gold Dealer

Gold dealers are responsible for selling the underlying physical gold of the project to token issuers or physical gold holders. Gold dealers generally need to hold a precious metals license/registration in the jurisdiction(s) where they operate and comply with local anti-money laundering and counter-terrorism financing (AML/CTF) requirements.

(4) Gold Custodian

The true value of tokenized gold lies in the physical gold stored in vaults; therefore, selecting an appropriate gold custodian is crucial. Project teams can consider having their gold custody services provided by vaults certified by the London Bullion Market Association (LBMA) or bank vaults, ensuring that these institutions have robust security and insurance arrangements. Given that gold-tokenization projects require third-party audits of the underlying gold, it’s also important to assess whether the custodians can support the audit requirements of both the project team and the auditor, and – where feasible – physically segregate the project’s underlying gold from the gold held for other clients of the custodian. If the gold tokenization project allows investors to redeem physical gold, it’s essential to ensure that the custodian can accommodate investors’ requests for physical redemption/delivery.

(5) Auditor

Investors’ confidence in gold tokens stems from whether the tokens are backed by sufficient physical gold. Therefore, project teams should select auditors with relevant qualifications and a solid reputation – such as independent third-party accounting firms – to periodically enter the vaults, conduct inventory checks, verify the quantity of physical gold and its corresponding serial numbers, and ensure that the on-chain records match the physical assets in the vault.

(6) Tokenization Technology Service Provider

Like other types of RWA projects, the project team must engage a tokenization technology service provider to offer services such as smart contract development for tokens, data transmission, blockchain node maintenance, and other technical services related to blockchain, smart contracts, and tokenization.

(7) Distributor

In addition to the issuer’s own distribution of tokens, project teams may consider engaging licensed distributors to distribute gold tokens, thereby reaching a wider investor base. Depending on the legal nature of the tokens, distributors may need to hold local financial licenses (such as the Type 1 (Dealing in Securities) license issued by the Securities and Futures Commission (SFC) in Hong Kong) and comply with local AML/CTF regulatory requirements. If the project team allows investors to subscribe for and redeem gold tokens using non-fiat currencies (such as stablecoins), it should also ensure that the distributors have the necessary capabilities and qualifications to provide such services.

3.2 Legal Nature of Tokens in Hong Kong

Depending on the token structure, gold tokens may fall under different product categories and thus be subject to different regulatory and compliance requirements in Hong Kong, including but not limited to:

(1) Securities: Gold tokens issued in the form of fund shares or structured notes will fall within the traditional definition of securities. In addition, project issuers should also consider whether the relevant arrangement constitutes a collective investment scheme under the Securities and Futures Ordinance (Cap. 571) (SFO), in which case the tokens would generally be treated as securities. The issuance and distribution of security tokens is subject to conventional securities regulatory frameworks, offering investors greater protection but potentially imposing higher compliance costs on the project. For example, a public offering of security gold tokens in Hong Kong may require the offering documents to comply with the relevant requirements under Section 105 of the SFO. Additionally, token distributors would typically be required to hold an SFC license to carry on Type 1 regulated activities (dealing in securities) and to comply with the SFC’s requirements applicable to the distribution of tokenized products.

(2) Virtual Assets: Even if gold tokens do not constitute securities, they may still fall within the definition of virtual assets, i.e., a cryptographically secured digital representation of value expressed as a unit of account or a store of economic value. The issuance and distribution of virtual assets is subject to the laws and regulations governing virtual assets in the relevant jurisdictions. In Hong Kong, depending on the distribution model and the target investors, the distribution of virtual assets may require an SFC Type 1 license (dealing in securities) and compliance with the SFC’s virtual-asset-related conduct requirements, and/or distribution through an SFC-licensed virtual asset trading platform. Once the dedicated licensing regime for virtual asset dealing services becomes effective, distributors may also be required to obtain such a license.

(3) Structured Products: If the redemption amount of a gold token is linked to the price or volatility level of gold, such gold tokens may fall under the definition of structured products. Structured products are a type of security, and in addition to the requirements applicable to conventional securities, the distribution of structured products also entails additional requirements relating to suitability assessments, risk profiling and enhanced risk disclosures.

3.3 Other Compliance Considerations for Issuing Tokenized Gold RWA in Hong Kong

(1) Fund Managers: If the project party chooses to place the underlying gold into a fund and tokenize the fund’s units/shares, the fund manager, which holds a license by the SFC to carry on Type 9 regulated activity (Asset Management), should engage with the SFC regarding the tokenization arrangement.

(2) Transparency of the redemption mechanism: To ensure investors’ rights and ensure investors fully understand the structure and risks of gold tokens, the project team should clearly and comprehensively disclose in the offering documents the redemption process and conditions, the method for calculating the redemption amount (or the quantity of physical gold deliverable), as well as the key risks associated with gold tokens.

(3) Blockchain Selection: As the critical infrastructure for minting, issuing, and redeeming gold tokens, issuers should carefully select a suitable blockchain, taking into account factors such as compatibility, security (e.g., resilience against 51% attacks and risks associated with code defects, vulnerabilities, attacks, and other threats), and the type of consensus mechanism.

(4) Smart Contract Audit: To mitigate cybersecurity risks associated with gold tokenization projects, in addition to engaging qualified and reputable tokenization service providers, project teams may also consider appointing an independent third party to audit the smart contracts prior to deployment.

(5) Personal Privacy and Cross-Border Data Transfers: The issuer shall ensure that the collection, processing, storage, and transfer (including cross-border transfer, where applicable) of investors’ personal data comply with the requirements of the Personal Data (Privacy) Ordinance (Cap. 486).

4. Overview of Major Gold Tokenization Projects

(1) Matrixdock (XAUm)

Matrixdock is an RWA brand under Matrixport. Its XAUm gold token showcases remarkable technical innovation and market fit in Asia. Each XAUm token corresponds to one troy ounce of LBMA-accredited gold with a minimum purity of 99.99%. Matrixdock provides an ‘Allocation Lookup’ feature for XAUm, enabling token holders to verify the specific details of the gold bar backing their tokens – such as the bar serial number and the refiner.

(2) Paxos Gold (PAXG)

PAXG is issued by Paxos Trust Company (Paxos). Paxos is a New York State-chartered limited-purpose trust company regulated by the New York State Department of Financial Services (NYDFS). PAXG operates under a trust-based structure, where each token represents a beneficial interest in a specific serial-numbered gold bar (allocated gold) held in a London vault. Similar to XAUm, token holders can log onto the Paxos website to obtain the corresponding serial number and other physical characteristics of the gold backing their PAXG. Through this structure, the underlying gold is intended to be held on a bankruptcy-remote basis from Paxos, thereby mitigating counterparty risk. Subject to applicable terms and eligibility requirements, investors may redeem PAXG for physical gold bullion bars.

(3) Tether Gold (XAUT)

XAUT is issued by Tether. Leveraging Tether’s extensive ecosystem built around USDT, XAUT has high market liquidity and broad exchange coverage. Under Tether Gold’s terms, each token represents an undivided interest in one fine troy ounce of on a specific bullion bar in the gold reserves held in custody. Following an investor’s purchase of XAUT, the custodian holds the corresponding gold in custody on behalf of token holders in accordance with the applicable terms.

(4) Alloyx (AUROX)

AUROX is issued by a BVI SPV under a Cayman-domiciled foundation (Axion Foundation). The token is a legally tokenized warehouse receipt backed by a direct beneficial interest in allocated physical gold bullion held in professional vault facilities (Brinks). The underlying gold is fully allocated and individually identifiable through bar serial numbers and related specifications, as disclosed in periodic reserve reports. The issuer legal structure is bankruptcy-remote. AUROX holders, subject to applicable compliance requirements and minimum thresholds, may redeem tokens for physical gold bullion across various locations globally. AUROX is designed to provide legally structured, transparent, and blockchain-transferable exposure to physical gold.

Conclusion

Gold RWA tokenization is not just a technological innovation, but also a new investment opportunity that lowers the investment threshold while preserving gold’s inflation-hedging characteristics. As Hong Kong accelerates its development as an international gold trading center, gold RWA tokenization may prove to be the ‘golden key’ that connects Hong Kong’s deep-rooted traditional finance ecosystem with a Web3-enabled future.

JunHe Virtual Assets & Web3 Team

We closely monitor regulatory developments worldwide relating to blockchain, virtual assets and real-world asset (RWA) tokenization, and have deep expertise and extensive practical experience across the relevant legal and compliance areas. Leveraging our strong technical capabilities and cross-border regulatory know-how, we have assisted a wide range of clients in successfully structuring and implementing more than ten RWA projects, covering diverse underlying asset types – including funds, bonds and cashflow/revenue rights – across multiple jurisdictions such as Hong Kong, Singapore, the Cayman Islands and the British Virgin Islands. Drawing on our ongoing work across different asset classes and cross-border transaction scenarios, we continue to engage with regulators, including the Securities and Futures Commission of Hong Kong, to help ensure our clients’ RWA projects proceed smoothly on a compliant basis, and to provide practical, replicable experience in support of the orderly and sustainable development of the RWA market.

We recommend that project sponsors intending to launch a tokenised gold RWA product in Hong Kong focus on the compliance of the project structure and make early preparations. If you have any questions regarding compliance for tokenised gold RWA offerings in Hong Kong, please feel free to contact us.

*With thanks to Zhou Ziyue for his contribution to this article

For further information, please contact:

QIAO, Zheyuan (Jacqueline), Partner, JunHe

zyqiao@junhe.com