8 June 2021

Electric vehicles are expected to dominate auto production in coming years. But signs ahead point to an industry shakeout. Here’s a starter to distinguishing value from hype.

The sounds of silence are filling the world’s highways.

Sales of electric vehicles* have been making huge inroads into the global automobile market over the past decade. Last year was pivotal, even amid the pandemic. Almost 3.2 million EVs were sold worldwide, representing a remarkable 40 percent growth year over year and 4.2 percent of all vehicle volumes. China and Europe drove the trend, accounting for approximately 85 percent of all EV purchases combined. By 2025, projected global sales of electric vehicles are expected to quadruple, reaching almost 15 million units.1

The rising trajectory of EV sales is powered by several factors: 1) Many governments have set regulatory mandates to curtail or eliminate production of internal combustion engine (ICE) vehicles; 2) customer acceptance of EVs is growing, fueled by increasing model availability, lower battery costs and improving range; and 3) major auto manufacturers are committing to EV development and production. For instance, many manufacturers, including Volvo, Honda, GM, and Mercedes, have already set target dates for going fully electric between 2030 and 2040.

Even as the EV market races ahead, questions about its profitability follow right behind. A crowded field of competitors and business models yet to be proven viable have both manufacturers and investors scratching their heads. Where should they invest their capital? When can they expect adequate returns?

A look at this fast-moving EV ecosystem provides a roadmap for distinguishing value from hype.

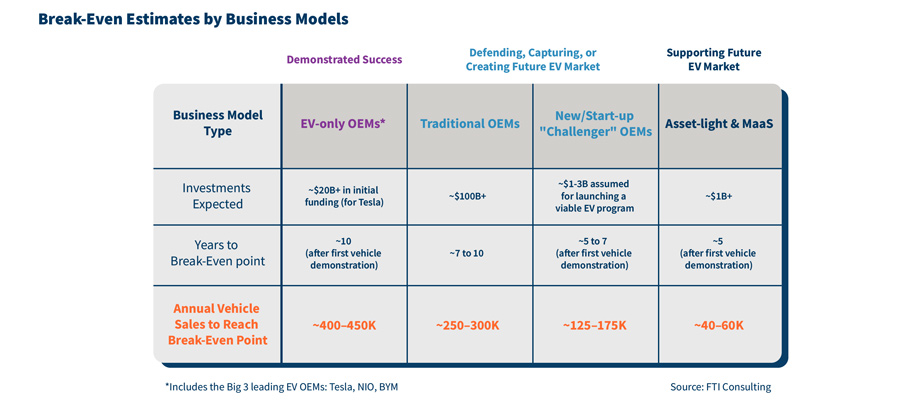

Four Strategies – Four Business Models

As the EV ecosystem evolves, many different business models are emerging in the original equipment manufacturing (OEM) space. The EV OEMs can be divided into four types:

-

Traditional OEM players ramping up EVs (e.g., BMW, GM, Ford, Toyota, Volvo, VW, etc.)

-

Asset-light and Mobility as a Service, or “MaaS” providers (e.g., Uber, Waymo, Fisker)

Each has its own major strategy and associated business model designed to capture a targeted portion of the emerging market with specific value propositions. Tesla, the early-to-market trendsetter, is focused on continuing its R&D to improve battery performance and building plants to continue to capture market share. Traditional players like GM and VW want to leverage their existing scale and automotive manufacturing assets to bring down costs and gain market share by appealing to a broader consumer base.

No matter the focus one thing all these OEMs have in common is the struggle to make a profit. Many are weighing the pros and cons of vertical integration as a strategy to control costs, increase potential margins and reduce supply risk. Approaches differ: Several global OEMs have announced the intent to control or invest in battery production (VW, GM, BMW); Toyota is outsourcing battery production and insourcing other components, like drivetrains; Tesla is fully vertically integrated; while Ford remains highly outsourced at the moment.2

Each has a different path to reach a break-even point for annual unit sales based on expected margins and invested capital.

Please click on the image to enlarge.

A Growing Valuation Bubble

In late March, President Biden announced “The American Jobs Plan,” a proposed $2 trillion spending package that focuses on U.S. infrastructure repair and upgrade. Among the bill’s goals is a $174 billion investment to “win the EV market.” That includes funding for building 500,000 charging stations, additional R&D investments and manufacturing EV batteries domestically. Although exact details of the bill remain under debate, Biden’s message is clear: Bet on a global EV future now.

As much as $250 billion of new capital has already poured into the industry over the past two to three years from sources like governments, OEMs and capital markets. Targeted segments include R&D, infrastructure, battery and other critical technology, but much of the funding is speculative as investors search for winners across a value chain that has shown little or no revenues to date.

The result is a huge valuation bubble.

More than 100 EV start-ups have received funding and many have astronomical valuations. Special purpose acquisition companies (SPACs) are highly active in this space, seeding a combined $100 billion in 26 MaaS tech companies in 2020. The SPAC frenzy continued in Q1 2021 with another dozen EV startups going public. More are expected this year.

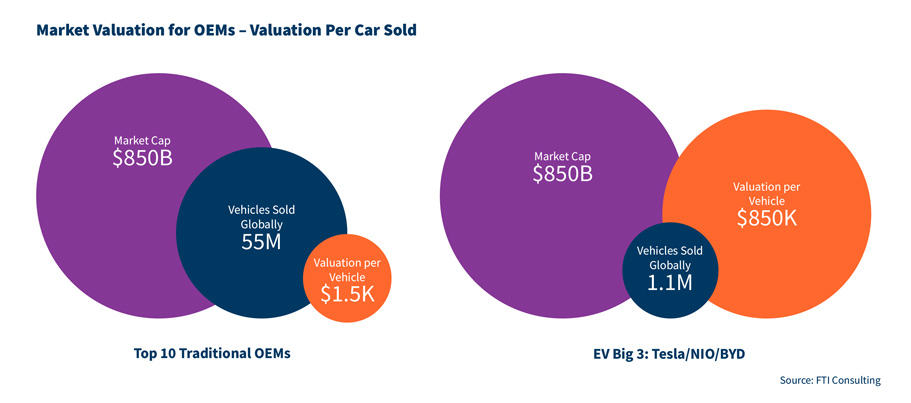

Meanwhile, the “EV Big 3” — Tesla, NIO and BYD — continue to cruise in the investor fast lane, reaching nearly $850B in market value as of the end of Q1. Remarkably, their market capitalization is almost identical to the top 10 traditional OEMs combined.

Just how hot is the EV Big 3 in investors’ eyes? Comparing global vehicle sales for the Traditional OEM and “EV Big 3” groups last year in relation to their respective market values offers deeper insight. With around 55 million units sold, the valuation per vehicle for the 10 traditional OEMs is $1.5K. By contrast, Tesla, NIO, and BYD sold less than 1 million units, resulting in a valuation per vehicle of a whopping $850K.3

Although investors may be leaning toward the newcomers at this point, the major OEM players aren’t standing still. They are deeply committed to keeping pace through large investments in retooling. Their competitive advantage lies in their assets and knowledge in design, long-time experience in building and selling automobiles, and wide network of dealerships and brand service centers.

The valuation bubble can best be glimpsed by looking at current market caps (as of March 31) for the OEMs with respect to the number of vehicles sold in 2020.4

Please click on the image to enlarge.

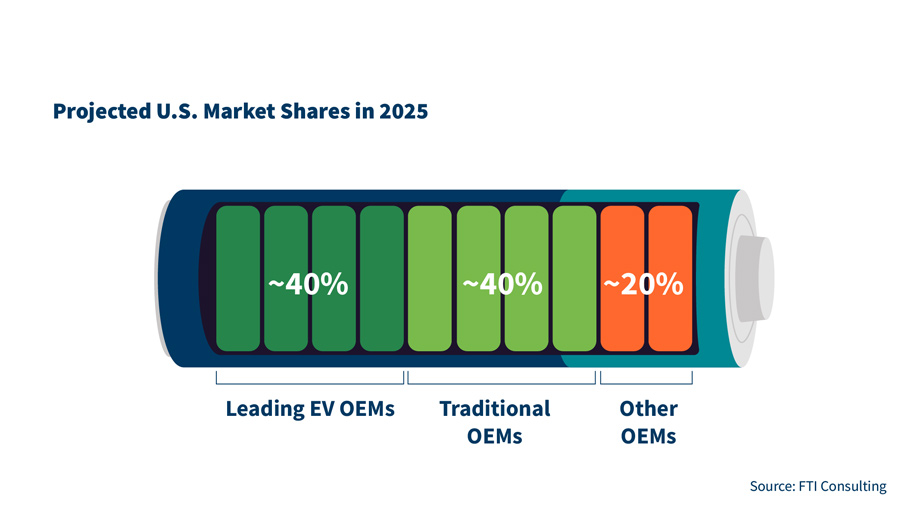

Survival of the Fittest – A U.S. View

In the United States, U.S. EV sales are expected to reach 1.6 million units by 2025 (less than 10 percent of total U.S. market volumes). The technological head start of pure EV companies like Tesla will allow them to hold a large share — likely more than 40 percent of that market. Traditional OEMs with major investments and dozens of EV model launches in the pipeline are expected to capture a similar share.5

That leaves less than 20 percent of the remaining market for all other players. It’s a tight squeeze for emerging nameplates today and for those that enter the market in the near future.

Please click on the image to enlarge.

Clearly, the market cannot absorb all that competition. Restructuring is sure to follow and likely the good niche players and nameplates will get consolidated into larger EV platforms. By 2030, we can expect to see fewer of the 2025 nameplates still on U.S. roads.6

Race to the Finish Line

The traditional OEMs have their sights set on transitioning from the internal combustion engine to electric in the coming decade. Balancing R&D, investment and capital allocation as they retool will be critical. For challengers, survival is more precarious and depends on finding the right partner and the optimal manufacturing strategy. How much capital will they need? What level of outsourcing and vertical integration will be appropriate?

Every automotive company will need to adapt rapidly to this new reality. There will be multiple laps and pit stops in the race toward profitability. Not every company will have what it takes for the long haul it takes to get to the finish line.

![]()

For further information, please contact:

neal.ganguli@fticonsulting.com

Footnotes:

* Includes battery-electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), and hybrid electric vehicles (HEVs)

1: Multiple sources: IHS Markit., Automotive News., FTI Consulting analysis.

2: Multiple sources: Automotive News., Just Auto., S&P Global.

3: Multiple sources: Jeffries., BloombergNEF., FTI Consulting analysis.

4: FTI Consulting analysis.

5: Multiple sources: IHS Markit., CNBC., FTI Consulting analysis.

6: FTI Consulting analysis.