Malaysia – Climate Accountability In Action: Why NSRF-Driven Disclosure Is Now A Business Imperative.

Introduction

In an era where climate accountability defines corporate credibility, Malaysian companies are under growing pressure to prove that their sustainability commitments are more than just words. First introduced on 24 September 2024 by the Securities Commission Malaysia, the National Sustainability Reporting Framework (“NSRF”) places this accountability into action requiring companies to disclose how climate risks and opportunities shape their strategy, performance, and governance.[1] The NSRF adopts the International Financial Reporting Standards (“IFRS”) Sustainability Disclosure Standards, specifically IFRS S2 or known as Climate-related Disclosures, as the national baseline for sustainability reporting in Malaysia, ensuring that climate information is transparent, comparable, and relevant to investors.[2]

By prioritising climate-first reporting, the NSRF compels boards and management to embed climate considerations into corporate decision and annual reports.[3] It’s no longer about compliance, but it’s about competitiveness, resilience, and investor confidence. In this new landscape, NSRF-driven disclosure has become a business imperative, one that determines not just how companies report, but how they lead in a climate-conscious economy.

This article explores the importance of NSRF implementation, its core principles under IFRS S2, the challenges faced by companies, and real examples of Malaysian corporates adopting climate-related disclosures in practice.

Importance of Implementing the NSRF through IFRS S2

The implementation of the NSRF is crucial in ensuring that Malaysian companies provide consistent, comparable, and decision-useful sustainability disclosures. By aligning with the IFRS S2, the NSRF enhances the credibility and transparency of corporate sustainability reporting. This alignment enables companies to communicate how climate-related risks and opportunities affect their business model, strategy, and financial performance, making them more attractive to global and domestic investors. Ultimately, it transforms sustainability reporting from a voluntary exercise into a strategic component of business and investment decisions, supporting capital access, competitiveness, and long-term resilience.

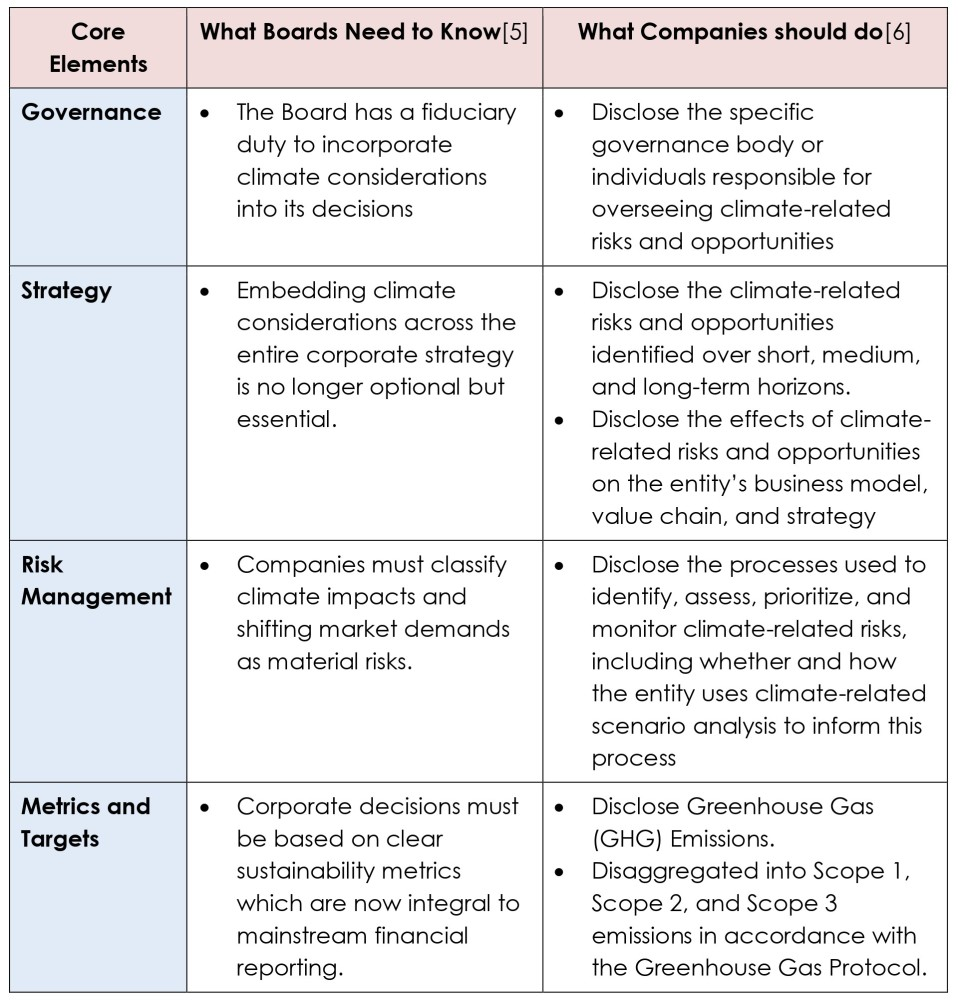

Furthermore, IFRS S2 strengthens corporate climate governance and risk management by requiring disclosures across four core areas, namely, governance, strategy, risk management, and metrics and targets. This structure compels boards and management to integrate climate considerations into their oversight and strategic planning, ensuring that companies are better equipped to anticipate regulatory, market, and environmental shifts. Such transparency also mitigates the risk of greenwashing by grounding sustainability claims in verifiable, data-driven reporting which can be seen as a key step toward building trust with investors, regulators, and the public.

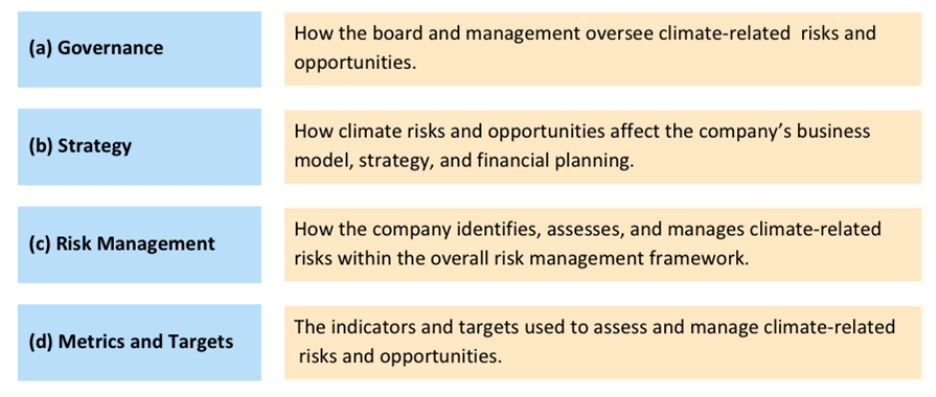

The Four Elements of IFRS S2

The NSRF adopts the IFRS Sustainability Disclosure Standards as the baseline standards for sustainability reporting in Malaysia. Under IFRS S2, the climate-related disclosure requirements are structured around four core elements[4]:

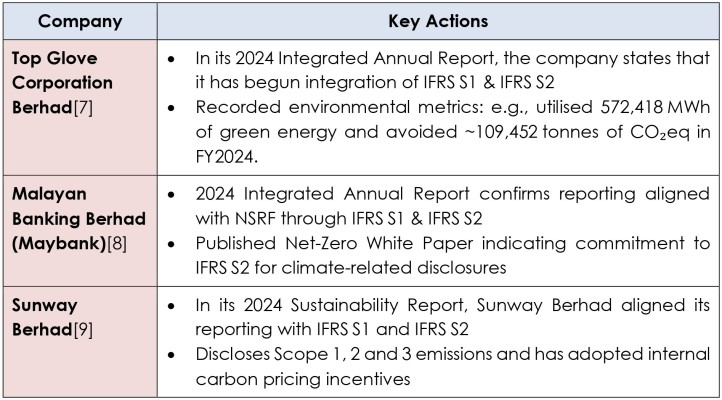

Leading by Example: Malaysian Corporates Adopting Climate‑Related Disclosures

These leading Malaysian companies are proactively implementing NSRF through IFRS S2 which shows a clear commitment to transparency and climate accountability for their stakeholders:

Challenges in Implementing NSRF

Implementing NSRF-driven climate disclosures presents several significant challenges for Malaysian companies. The primary obstacle would be difficulty in obtaining reliable emissions data, particularly for Scope 3.[10] These indirect emissions, originating from activities outside a company’s control, such as supply chain operations, product usage, transportation, waste management, requires extensive collaboration with external parties and the exchange of robust data. Consequently, organization often must implement new systems and reporting tools to manage this complexity.

Furthermore, a significant skills gap adds to these challenges. Most of board members and senior leadership teams lack the technical expertise required for key responsibilities such as conducting climate scenario analysis and evaluating the financial implications of climate-related risks.[11] Organizations also continue to face difficulties in integrating sustainability considerations into strategic planning, risk management frameworks, and external reporting processes. Addressing these gaps is essential to ensure that NSRF through IFRS S2 disclosures are robust, credible, and capable of meeting investor expectations.

Initiative to Overcome Reporting Barriers

(a) Summary Guide for Board[12]

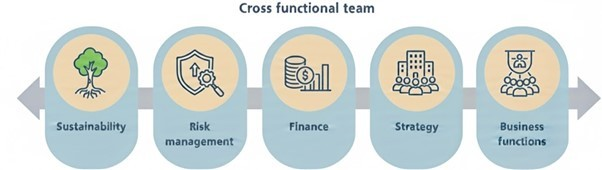

Securities Commission has introduced an NSRF guidelines for Boards to implement the IFRS S1 and S2 in disclosing any climate related issues in company’s respective sustainability report. This simplified guide helps the Board to understand the essential steps in preparing a sustainability report, including aligning sustainability data with financial reports, integrating climate risks into company risk management, and preparing for external review. Furthermore, the guide elaborates on the importance of proper governance and the establishment of a cross-functional team to ensure a whole-of-organisation and integrated approach.

The guide reinforces that although the “tone from the top” set by the board is critical, the active involvement and support of other teams and internal stakeholders are fundamental to embedding these practices across the company.

(b) Policy, Assumptions, Calculators and Education (“PACE”)[13]

The Securities Commission Malaysia has introduced an effective way to address the reporting challenges under the NSRF, namely the PACE initiative. PACE offers companies policy guidance, emissions‑calculator tools, and structured training programmes to help companies gradually adopt the framework. One of the key tools mentioned is an emissions calculator, which helps companies measure and report their greenhouse gas emissions including the challenging Scope 3 emissions that come from suppliers, product use, transportation, and waste.

Conclusion

In conclusion, the NSRF is a major push to make Malaysian businesses more transparent and prepared for a future shaped by climate risks. The urgency is now clear as Bursa Malaysia has made these disclosures mandatory.[14] By aligning with the global IFRS S2 standard, it ensures that climate reporting is not just a procedural obligation but provides real, effective decision information for investors and the public.

For further information, please contact:

Norhisham Abd Bahrin, Partner, Azmi & Associates

norhisham@azmilaw.com

- “National Sustainability Reporting Framework to Enhance Sustainability Disclosures – Media Releases,” Securities Commission Malaysia, last modified September 24, 2024, https://www.sc.com.my/resources/media/media-release/national-sustainability-reporting-framework-to-enhance-sustainability-disclosures.

- “National Sustainability Reporting Framework,” Securities Commission Malaysia, accessed November 14, 2025, https://www.sc.com.my/nsrf.

- Bursa Malaysia, Main Market Listing Requirements: Paragraph 29 in Part A, paragraph 14 in Part C and paragraph 15 in Part E, of Appendix 9C; as well as paragraphs 1.2A and 6.1A of Practice Note 9 and Practice Note 9A and ACE Market Listing Requirements, Paragraph 30 in Part A of Appendix 9C; as well as paragraphs 1.2A and 6.1 of Guidance Note 11 and Guidance Note 11A of the ACE LR.

- “Navigating the Financial Sector’s Transition to the National Sustainability Reporting Framework,” Bank Negara Malaysia, last modified 2024, https://www.bnm.gov.my/documents/20124/17523783/fsr24h2_en_box3.pdf.

- Chapter Z. Mexico, “Board Dialogues on Climate Governance,” Climate Governance Hub Climate Governance Initiative, last modified October 7, 2025, https://hub.climate-governance.org/article/board-dialogues-on-climate-governance.

- International Sustainability Standards Board, “IFRS S2 IFRS® Sustainability Disclosure Standard,” IFRS Sustainability, June 2023, https://www.ifrs.org/content/dam/ifrs/publications/pdf-standards-issb/english/2023/issued/part-a/issb-2023-a-ifrs-s2-climate-related-disclosures.pdf?.

- “Top Glove Integrated Annual Report 2024,” Top Glove Corporation Bhd, accessed November 14, 2025, https://tgapp.topglove.com/IAR/2024/Integrated_AR_2024/Interactive_PDF/.

- “Maybank Integrated Annual Report 2024,” Malayan Banking Berhad, last modified 2024, https://www.maybank.com/iwov-resources/documents/pdf/annual-report/2024/Maybank-AR2024-Integrated-Annual-Report.pdf?.

- “Sunway Sustainability Report 2024,” Sunway Sustainability Report, last modified October 23, 2025, https://sustainability.sunway.com.my/?.

- “Greenhouse Gas Emissions Disclosure requirements applying IFRS S2 Climate‑related Disclosures,” IFRS Sustainability, last modified May 2025, https://www.ifrs.org/content/dam/ifrs/publications/pdf-standards-issb/english/2023/issued/.

- “Board Members See Improvement Opportunities in Climate Skills and Governance Within Sustainability Strategies,” WTW, last modified July 14, 2023, https://www.wtwco.com/en-ie/insights/2023/07/board-members-see-improvement-opportunities-in-climate-skills-and-governance-within-sustainability.

- Securities Commission Malaysia, “NATIONAL SUSTAINABILITY REPORTING FRAMEWORK Navigating the Transition: A guide for boards,” January 2025, https://www.sc.com.my/api/documentms/download.ashx?id=972d92d8-b7c4-4b9d-a077-0b2fcba3584e.

- “National Sustainability Reporting Framework,” Securities Commission Malaysia, accessed November 14, 2025, https://www.sc.com.my/nsrf.

- Bursa Malaysia, “BURSA MALAYSIA REQUIRES SUSTAINABILITY REPORTING USING THE IFRS SUSTAINABILITY DISCLOSURE STANDARDS Enhancements reflect the National Sustainability Reporting Framework,” Bursa Malaysia, last modified December/January 23, 2024, https://www.bursamalaysia.com/sites/5bb54be15f36ca0af339077a/content_entry5c11a9db758f8d31544574c6/6768e229e6414a4ba0eb9f4d/files/23122024__MEDIA_RELEASE_BURSA_MALAYSIA_REQUIRES_SUSTAINABILITY_REPORTING_USING_THE_IFRS_SUSTAINABILITY_DISCLOSURE_STANDARDS.p.