29 January, 2020

The world’s private wealth needs a safe home especially with volatile and uncertain economies. The increasing number of ultra-high net worth individuals and family offices need good independent advice and practical bespoke solutions that address their needs and concerns, as opposed to buying standard wealth management or insurance products sold by financial institutions.

Also, as entrepreneurs and patriarchs/matriarchs age, they will look into wealth succession. It is common knowledge that many from the second and third generations of such families do not wish, or are not equipped, to take over the wealthy family businesses. Many of the younger generation of entrepreneurs may be educated in the West or have exposure to western wealth preservation structures, including trusts and family offices. In addition, the migration of wealth and professionals from the West to Asia, for one reason or another, has also created a great platform and impetus for the wealth management industry.

Singapore presents itself as a very attractive and viable option, as a widely respected international financial centre with genuine and substantive business activity and a thriving economy. The wealth management and trust infrastructure and professionals within Singapore provide a one-stop solution for private clients.

Key Objectives of Private Clients for Wealth Planning

Private clients have a number of objectives when it comes to wealth planning but we can distil several common objectives. These are mitigation of taxes and estate duties, protection of wealth, transition of wealth and authority to the next generation, creation of a legacy, and more importantly, privacy.

It is worth mentioning that there are private clients who have expressed their unreserved love for their children, but not necessarily entirely endorsing their children’s choice of spouses or partners. Private clients tend to have a desire to protect their assets from their in-laws. As such, structures and solutions will have to be put in place to ensure the assets are adequately ring-fenced from not just creditors but also people living under the same roof. Another key objective seems to be privacy of the family and family wealth. Typically, neither the giver of the wealth and power, nor the recipients of such, wish to have the public know how much wealth and power are involved.

The key concerns of private clients would be to have a sustainable structure that provides confidentiality, flexibility and protection. Even though there are various tools and structures that can be used for wealth planning – including wills, lasting powers of attorney, insurances, offshore companies and foundations – we see the increasing employment of trusts used for such purposes. In recent years, many developed countries have frowned upon offshore centres in places like the Caribbean, complicated structures and multi-jurisdictional offshore companies. Major leaks of confidential private client data over the years in scandals like the Panama Papers have not just embarrassed private clients but also the private banks and advisers involved. “Offshore” has since taken on a more contentious and, albeit unfairly so, sinister connotation.

Private Trusts, a Viable Solution

A private trust might be new to some Asian private clients who are not familiar with the common law system or the concept of trust. The very fact that a rich private client is asked to transfer a substantial portion of his wealth or assets to a stranger (albeit a professional or licensed trust company), to lose control over such wealth or assets, and to pay an inception fee for setting up, and professional fees for the operation of, the trust does not make much sense at first. However, once the private client fully appreciates the benefits of a private trust and how it works for him and the beneficiaries he wishes to bless, the decision is quite easily reached.

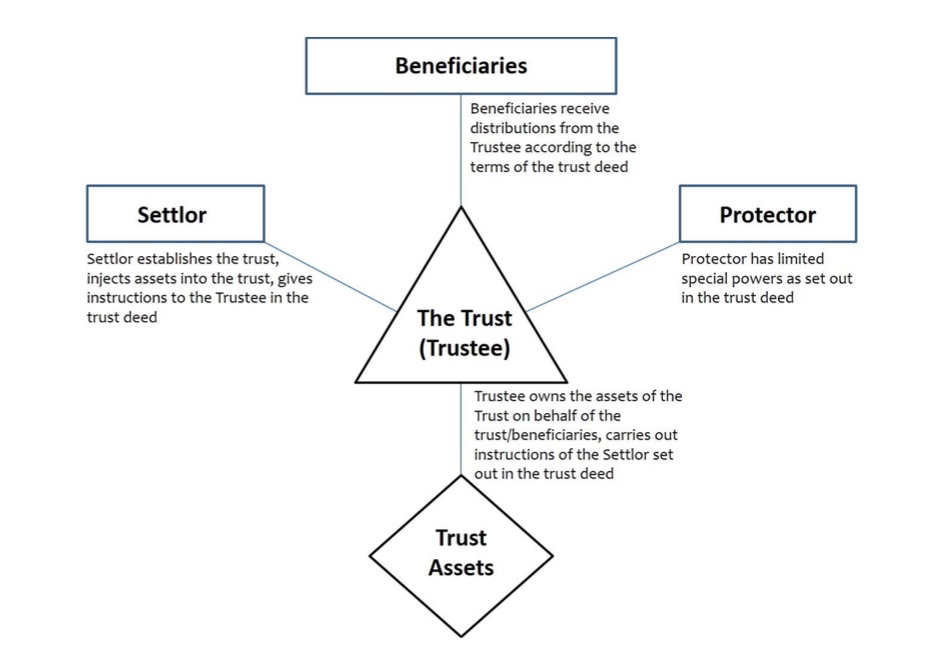

A private trust is a legal arrangement, and not a separate legal entity, that requires a trustee to be the legal-owner of all trust assets and enter into all contracts on behalf of the trust. The trustee has specific duties under the Trustees Act, Cap. 337 of Singapore (“Trustees Act”) and common law. Professional trustees are also licensed and regulated by the Monetary Authority of Singapore (“MAS”) under the Trust Companies Act, Cap. 336 of Singapore (“Trust Companies Act”). The beneficiaries of the trust must be specific or part of an identifiable class (e.g. my child no.1 and child no.2; or my legal children and grandchildren).

Please click on the image to enlarge.

The trust can be revocable or irrevocable (e.g. the trust can be amended and terminated anytime; or the trust cannot be amended or terminated at all). The manner in which the trust assets can be dealt with are fairly flexible, but must be spelt out clearly in the trust deed. Under Singapore's trust law, the settlor (i.e. the one creating the trust and putting his/her wealth and assets into the trust) of a trust can retain limited powers (including the powers to direct the trustee on how to invest the trust assets) in the trust.1 Although the Singapore legislation makes no mention of the office of the protector (akin to an independent guardian of the trust, with powers over very limited but major issues like changing the trustee or domicile of the trust), a protector can also be appointed as an additional safeguard. There are also favourable tax incentives available for certain types of Singapore trust, which we will not cover in this article (but do get in touch with us if you would like to find out more).

Meeting the Clients’ Needs

In a private trust, assets of the settlor are legally transferred to the trustee and thus ring-fenced against creditors and third parties. This will give the private client peace of mind.

The professional institutional trustees in Singapore must be licensed under the Trust Companies Act2 and are subject to stringent licensing requirements and ongoing supervision by the MAS. They are also subject to stringent duties and obligations under the Trustees Act3 and common law. The assets in the trust set up by the

private client are also required by law to be segregated from the trustee’s own assets and the assets in other trusts operated by the trustee. These provides additional comfort and protection for the private client and the beneficiaries.

As a private trust allows the flexibility of adding or removing beneficiaries from the trust, the private client can grant the trustee discretion within certain parameters to include deserving beneficiaries and exclude undeserving beneficiaries that should be excluded. The private client can also keep things fluid by identifying only a certain class of beneficiaries and leaving it to the trustee to determine later which persons should be included or excluded from the distributions. The quantum of distributions can also be flexible and left to the discretion of the trustee to determine, based on the circumstances at the relevant time. The private client can also specify conditions for the beneficiaries to receive payments under the trust, for example when the beneficiary attains his/her first university degree, gets legally married or reaches a certain age.

Since the settlor can retain limited powers in the trust, there is legitimacy for private clients to have some measure of control over matters without the trust being deemed a sham, provided the powers retained are not so extensive and wide-ranging that the settlor is deemed to be in de facto control of the entire trust.

In addition, Singapore offers other solutions for private clients.

A Singapore foreign trust, for purposes of the nation’s income tax law, is a foreign trust created in writing with no Singapore settlor and beneficiary4. This means that neither the settlor nor any of the beneficiaries can be a citizen or resident of Singapore. In the case of companies, they must be foreign companies5 whose beneficial owners are all non-Singapore citizens and non-residents of Singapore. Such a trust can enjoy favourable tax treatment under our tax regime including tax exemption for specified income from designated investments6. Another key condition is that the trustee must be licensed under the Trust Companies Act7.

Singapore also allows the use of private trust companies, private unit trusts, single investor funds or private label funds (where a private fund is set up exclusively for the family), family offices and family-owned investment companies. These are different structures that are available but require proper and detailed planning to extract the benefits of the structure for the private client’s needs.

Conclusion

In short, with regard to wealth management, Asia is the place to be for now and the foreseeable future. The wealthy will find that they will increasingly require more sophisticated independent bespoke advice and solutions for their diverse and specific needs. With the current trust law and structures in place to address such needs and concerns, the wealth management industry in Singapore is well placed to meet the increasing challenging demands of private clients.

Tan Woon Hum, Partner, Shook Lin & Bok

woonhum.tan@shooklin.com

1 Section 90 (5) of the Trustees Act states that no trust or settlement of any property on trust shall be invalid by reason only of the person creating the trust or making the settlement reserving to himself any or all powers of investment or asset management functions under the trust or settlement.

2 Section 3 of the Trust Companies Act.

3 Such the statutory duty of care provided for in Section 3A of the Trustees Act.

4 Regulation 2A of the Income Tax (Exemption of Income of Foreign Trusts) Regulations ("Income Tax Regulations"). 5 As defined in Regulation 2 of the Income Tax Regulations.

6 Regulation 3 of the Income Tax Regulations.

7 Ibid.