23 July 2021

This update provides an overview of key regulatory developments in the past three months relevant to companies listed, or planning to list, on The Stock Exchange of Hong Kong Limited (HKEx), and their advisers. In particular, it covers amendments to the Rules Governing the Listing of Securities on HKEx (Listing Rules) as well as announcements, guidance and enforcement-related news from HKEx and the Securities and Futures Commission (SFC). Other recent market developments may also be included. We do not intend to cover all updates that may be relevant, but we welcome feedback, so please contact us if you’d like to see analysis of other topics in the future.

-

HKEx Consults on Corporate Governance Code and Related Listing Rules

-

HKEx Consults on Reforms To Enhance Listing Regime for Overseas Issuers

-

SFC and HKEx Publish Joint Statement on IPO-related Misconduct

-

HKEX Publishes Consultation Conclusions on Profit Requirements

-

HKEX Publishes Consultation Conclusions on Disciplinary Powers and Sanctions

-

Takeovers Bulletin: Additional Disclosure of Future Intentions for Unlisted Securities

HKEx Announces Move to T+2 IPO Settlement Under FINI Plan

HKEx has announced that it will proceed moving IPOs to a “T+2” settlement timetable under its “Fast Interface for New Issuance” (FINI) plan. This shift is a slight change to the original T+1 settlement plans proposed in the HKEx concept paper published in November 2020, but nevertheless a significant improvement on the current process, which generally results in IPOs in Hong Kong settling on a T+5 basis.

The plan will require IPOs to follow the new T+2 timetable unless a company obtains a waiver from HKEx. The new timetable requires that:

-

pricing must occur by 12 p.m. Hong Kong time on the pricing date (day “T”);

-

underwriters must submit placee lists to HKEx on the morning of the day after pricing (“T+1”), with the allotment results announcement posted and listing approval obtained the same day; and

-

listing will take place and trading commence the following morning (“T+2”).

The plan also provides for a new public offer pre-funding mechanism that aims to avoid the lockup of large amounts of funds during the public offer period of popular IPOs, as well as for a new investor identification requirement to manage multiple applications. HKEx also proposes introducing a new online platform accessible by market participants to handle subscription, pricing, allotment, payment, listing approval and stock admission.

HKEx will make amendments to the Listing Rules and CCASS rules to implement the reforms, which will likely be subject to a separate consultation process. The forms of legal documentation (such as underwriting agreements, receiving banks agreements and share registrar agreements) commonly adopted by the market will also require corresponding changes.

Pilot group testing of the new system is expected to begin in Q2 2022, with a full launch scheduled to occur in December 2022 at the earliest.

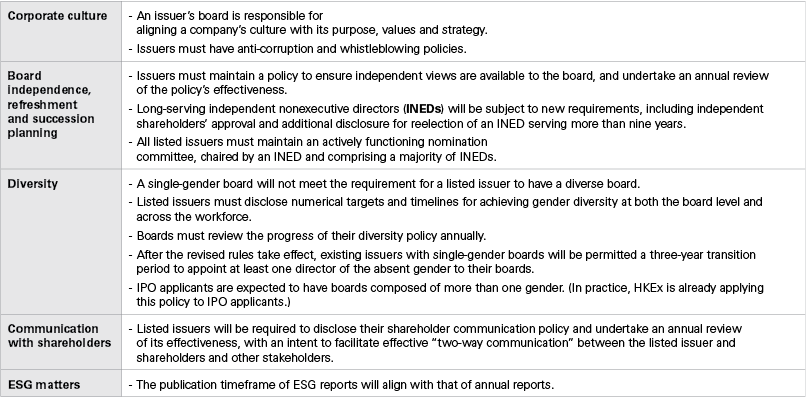

HKEx Consults on Corporate Governance Code and Related Listing Rules

HKEx published a consultation paper on April 16, 2021, outlining proposed enhancements to corporate governance regulation and reporting. The proposals include measures to further enhance corporate governance standards among listed issuers in Hong Kong, specifically in the areas of corporate culture, director independence, diversity, and environmental, social and governance (ESG) disclosures and standards.

Key proposals include the following:

Please click on the image to enlarge

HKEx also proposes rearranging the Corporate Governance Code to improve its organization and readability, in order to further facilitate issuers’ compliance and adoption of high standards in corporate governance.

HKEx Consults on Reforms To Enhance Listing Regime for Overseas Issuers

HKEx is proposing to streamline its listing regime for overseas companies to open new opportunities for those companies to list in Hong Kong. The proposals, released in a consultation paper published on March 31, 2021, will for the first time permit Greater China issuers to undertake secondary listings in Hong Kong regardless of the industry in which they operate, as well as allow certain issuers with noncompliant dual-class share structures to undertake dual primary listings. The key proposals include the following features.

More Flexibility for Dual Primary Listings With WVR and VIE Structures

Under existing rules, Grandfathered Greater China Issuers (i.e., issuers with a center of gravity in Greater China and listed overseas on or prior to December 15, 2017) or Non-Greater China Issuers with noncompliant weighted voting rights (WVR) and/or variable interest entity (VIE) structures were only permitted to undertake a secondary listing in Hong Kong. Under the new proposals, these companies will be allowed to apply directly for a dual primary listing while retaining their existing noncompliant structures, as long as they (i) meet the requirements for being an “innovative company,” (ii) have a track record of good regulatory compliance of at least two full financial years, and (iii) either have a minimum market capitalization of (a) at least HK$40 billion or (b) at least HK$10 billion with revenue of HK$1 billion for the most recent financial year.

HKEx proposes that if such a company subsequently voluntarily delists from its overseas exchange, thereby retaining its sole primary listing in Hong Kong, it may still retain its noncompliant WVR or VIE structure.

Expansion of Secondary Listing Regime for Greater China Issuers Without WVR Structures

Existing HKEx practice has not permitted Greater China-based companies to undertake secondary listings in Hong Kong unless they fell within the “innovative company” regime introduced in 2018. Now HKEx proposes an expansion of the secondary listing regime to permit a company (including those based in Greater China) that do not have a WVR structure to conduct a secondary listing in Hong Kong regardless of whether the business is an “innovative company,” provided it can demonstrate a minimum market capitalization of (i) HK$3 billion (with a track record of good regulatory compliance for five full financial years on the New York Stock Exchange (NYSE), Nasdaq or the London Stock Exchange (LSE) for Greater China companies, or on a wider range of recognized overseas exchanges for other companies); or (ii) HK$10 billion (with a track record of good regulatory compliance for two full financial years on the NYSE, Nasdaq or the LSE). These proposed criteria will not apply to companies with a WVR structure that will continue to be subject to the existing requirements.

In addition, all secondary listed issuers will become subject to the requirement to convert their listing to a primary listing if the majority of trading volume in their shares migrates to HKEx (this requirement currently applies only to Greater China issuers). If a secondary listed issuer is delisted from its primary exchange, it will be treated as primarily listed in Hong Kong. In both cases, the company will then lose the benefit of the waivers granted to secondary-listed companies.

Single Set of Shareholder Protection Standards

The rules for listing of overseas companies on HKEx have developed over years and the related listing requirements have become scattered in various places in the Listing Rules, the joint policy statement regarding the listing of overseas companies (JPS) and guidance letters published by HKEx. This has resulted in a fragmentary and unnecessarily complex regulatory framework for overseas companies listing in Hong Kong. HKEx now proposes streamlining the shareholder protection standards for all issuers regardless of the place of incorporation, replacing all of the existing rules with a single set of “Core Standards.” The Core Standards will apply to all companies, including those incorporated in Hong Kong and the People's Republic of China (PRC), and will effectively render Hong Kong “jurisdiction-neutral” in terms of place of incorporation for listing applicants. Companies that are already listed will also be required to comply with the Core Standards.

Notable provisions among the 14 proposed Core Standards include the following:

-

Shareholders can remove directors with a simple majority vote. (Limited exemptions from this requirement may be available to certain WVR issuers.)

-

Companies must hold an annual general meeting every year.

-

Shareholders holding at least 10% of voting rights (on a one-share, one-vote basis) have the right to convene a shareholders meeting and add resolutions to a meeting agenda.

-

Shareholders have the right to speak and vote at general meetings.

-

A 75% (or, for PRC companies, two-thirds) majority vote of shareholders is required to amend the constitutional documents of a company, to change the rights attached to any class of shares or to wind up the company.

-

The Hong Kong branch register of shareholders must be open to inspection.

SFC and HKEx Publish Joint Statement on IPO-related Misconduct

The SFC and HKEx have issued a joint statement on regulatory issues in recent new listings, seeking to address issues that may undermine development of an open, orderly and fair market, or impact the integrity of Hong Kong’s capital market and reputation as an international finance center.

Regulators highlighted three specific concerns:

-

An increase in “pump-and-dump” schemes, commonly orchestrated at early stages of the IPO process and associated with the IPOS of small market cap companies. In these schemes, disingenuous parties manipulate the market to inflate share prices and induce unwary investors to purchase the shares, and then “dump” the shares on the market at an artificially high price.

-

Lack of transparent share placement and price discovery processes. This results when companies allocate shares in an IPO placing tranche to controlled placees in order to (i) artificially satisfy the initial listing requirements under the Listing Rules, creating a false market for the shares, or (ii) corner/restrict the shares to facilitate market manipulation after the shares are listed. In such cases, how the placees were identified, the basis for allocating shares in the placing tranche and how the IPO price was determined can all also be unclear.

-

Payment of unusually high underwriting commissions and other suspicious compensation arrangements involving underwriters. Regulators noted an increase in the average underwriting commission rate for IPOs with market capitalizations below HK$600 million from 4% in 2017 to 12% in 2020.

The regulators believe some listing applicants would not have satisfied initial listing requirements without such arrangements. Further, the IPO price and valuation might be substantially lower than that stated in the prospectus, in some cases resulting in a substantial drop in share price on the first day of trading to a level more closely reflecting the true market value of the company.

The regulators identified a list of features that may prompt them to make further inquiries regarding a new listing. These include a market capitalization that barely meets the minimum thresholds, a very high P/E ratio, unusually high underwriting commissions or listing expenses, and a concentration of shareholdings with a limited number of shareholders. The regulators stated that they may reject a listing application if questions raised are not satisfactorily addressed, or if any basic listing or suitability requirements are not met. Further, the regulators may investigate intermediaries involved in problematic IPOs and suspend dealings where they find unusual movements in share prices or high concentration of shareholdings.

HKEX Publishes Consultation Conclusions on Profit Requirements

Following HKEx’s consultation paper on the main board profit requirement (which was covered in our Hong Kong Regulatory Update published in December 2020), the exchange has announced its consultation conclusions with the amended Listing Rules to take effect starting January 1, 2022.

Under the amended rules:

-

the listing requirement for profit attributable to shareholders in respect of the most recent financial year is increased from HK$20 million to HK$35 million;

-

the profit requirement for the two preceding financial years in aggregate is increased from HK$30 million to HK$45 million; and

-

in the case of a spin-off, the parent, excluding its interest in the company being spun off, must have an aggregate profit attributable to shareholders of not less than HK$80 million (increased from HK$50 million) in respect of any three out of the five financial years immediately preceding the spin-off application.

HKEX Publishes Consultation Conclusions on Disciplinary Powers and Sanctions

New amendments to the Listing Rules expanding HKEx’s disciplinary powers and sanctions came into effect on July 3, 2021. These amendments implement, with only minor modifications, the proposals set out in the relevant HKEx consultation paper (which was covered in our Hong Kong Regulatory Update published in September 2020).

Key amendments now implemented include:

-

Secondary liability for Listing Rules breaches: The scope of HKEx disciplinary powers extends to include senior management (broadly defined) of listed companies and their subsidiaries, as well as substantial shareholders, financial advisors and other professional advisors (including accountants and lawyers). The exchange may impose secondary liability on these parties if they have caused a contravention of the Listing Rules by action or omission or knowingly participated in a contravention.

-

Broadened scope of prejudicial statements: HKEx can now in a broader variety of circumstances issue a statement that the retention of office by a particular individual is prejudicial to the interests of investors, and the exchange may impose additional sanctions — including the denial of market facilities to the company involved, suspension or delisting — if the relevant individual remains in office.

-

Disclosures of disciplinary action: Listed issuers are required in their annual reports to disclose full details of any public sanctions made against current or proposed directors and members of senior management.

-

Introduction of Director Unsuitability Statements: As a new form of sanction, HKEx may issue “Director Unsuitability Statements,” which are public statements that a director is unsuitable to be a director or senior management member of a named listed issuer. The statements represent a serious sanction that will be reserved for the most severely compromising conduct and breaches.

Takeovers Bulletin: Additional Disclosure of Future Intentions for Unlisted Securities

In its most recent Takeovers Bulletin, the SFC has advised that it will require companies offering unlisted securities as consideration in a takeover offer to state whether they intend to seek a listing of those securities (or of the business of the offeree company in question) in the future, and if so, on which exchange.

The SFC noted the increasing trend of offering unlisted securities as consideration for the shares of an offeree company, especially when a privatization proposal is involved. Currently in a securities exchange offer, especially where unlisted securities are offered, Schedule 1 of the Takeovers Code requires additional disclosures about the securities being offered, including information relating to the value of the offeror’s securities, business operations and latest financial position.

The SFC emphasized General Principle 5 of the Takeovers Code, which provides for offerees to make an informed decision based on sufficient information, advice and adequate time frame for deliberation, and that all relevant information be provided to offerees. The new disclosure requirements are intended to help achieve the aims of this principle.

Enforcement Matters

HKEx Censures and Criticizes Coslight and Its Directors for Failure To Comply With Listing Rules Requirements for Notifiable Transactions

HKEx has censured a listed company for multiple breaches of the Listing Rules regarding notifiable and connected transactions.

Coslight Technology International Group Limited (Coslight) engaged in the following transactions, which involved Listing Rules breaches:

-

Between July 2017 and May 2018, Coslight’s non-wholly owned subsidiary disposed all of its equity interest in its own wholly owned subsidiary through two transactions, each of which constituted a major transaction and together constituted a substantial disposal. Coslight failed to comply with the reporting, announcement and shareholders’ approval requirements for these transactions.

-

In September 2018, Coslight disposed of its equity interest in another non-wholly owned subsidiary through a substantial disposal, for which the circulation and shareholders’ approval requirements were only completed after the transaction occurred.

-

In November 2018, Coslight’s non-wholly owned subsidiary entered into a disclosable transaction for which the announcement was not made until more than three months after completion of the transaction.

-

In September 2020, Coslight acquired an equity interest in a company from a connected person and failed to comply with the relevant reporting and announcement requirements.

HKEx censured and criticized Coslight for (i) noncompliance with the Listing Rules regarding notifiable and/or connected transactions and (ii) deficient internal controls. Ten of the company’s current and former directors were found to have breached their directors’ undertakings to use their best efforts to ensure Coslight complied with the Listing Rules. HKEx directed the relevant directors to attend training and required Coslight to appoint an independent professional adviser to conduct an internal control review and an independent compliance adviser to oversee Coslight’s ongoing compliance with the Listing Rules.

HKEx Censures Yu Tian and Its Directors for Failure To Comply With Listing Rules Requirements for Connected Transactions

HKEx censured China Yu Tian Holdings Limited (Yu Tian), and seven current and former directors, for their failure to publish an announcement and seek independent shareholders’ approval for a connected transaction.

Between January 2018 and April 2018, Yu Tian and its subsidiary granted two loans to parties connected to executive directors Ms. Xuemei Wang and Mr. Wang Jindong, respectively. The loans were issued interest-free and without collateral, but personally guaranteed by Ms. Wang. They allegedly served as additional compensation to Ms. Wang and Mr. Wang, and were purportedly approved by the directors verbally without any documentation.

Yu Tian neither published an announcement nor sought independent shareholders’ approval for this transaction. Additionally, Ms. Wang and Mr. Wang took an active role in the proposal, approval and execution of the loans, despite their conflicts of interest.

Other directors failed to convene a board meeting to discuss the loans and to properly benchmark the remuneration of Ms. Wang and Mr. Wang. The directors were therefore found to have breached their undertakings to use their best efforts to procure Yu Tian’s compliance with the Listing Rules.

HKEx Censures and Criticizes Tenwow and Its Directors for Failure To Comply With Listing Rules Requirements for Connected Transactions and Inadequate Internal Controls

HKEx censured Tenwow International Holdings Limited (Tenwow) and five of its executive directors, and criticized four nonexecutive directors, for breaching the Listing Rules requirements for connected transactions and for failure to establish effective internal controls.

In 2017, a subsidiary of Tenwow entered into a credit line contract with a bank that provided financial assistance to a company connected to the then executive director and CEO of Tenwow, Mr. Lin Jianhua (a connected person of Tenwow). As a connected transaction, the credit line contract was subject to the requirements under the Listing Rules regarding announcement, circulation and independent shareholders’ approval, with which Tenwow failed to comply.

Further, Mr. Lin executed the credit line contract on behalf of Tenwow even though the transaction had not been approved by the board of directors. By doing so, he acted with a conflict of interest. The transaction did not confer any benefit to Tenwow, and instead prejudiced Tenwow’s interests. HKEx thus found Mr. Lin to be in breach of his requirement to fulfill fiduciary duties and duties of skill, care and diligence in his performance as a director.

Investigations into prepayment agreements between Tenwow’s subsidiaries and suppliers also revealed serious deficiencies in Tenwow’s internal controls. For example, the subsidiaries had made payments to suppliers without collecting supporting documents, and an executive director had signed payment documents on behalf of Mr. Lin without making inquiries into the identity of the payees or the purpose of the payments.

HKEx thus found that each of the directors failed to use his best efforts to ensure that Tenwow had effective internal controls, and found the directors to be in breach of their pledge to HKEx due to their failure to comply with and to ensure Tenwow’s compliance with the Listing Rules.

Tenwow had also failed to publish various interim and annual results and reports between June 2018 and June 2019, as required by the timelines stipulated by the Listing Rules. HKEx suspended Tenwow’s stock in 2018, placed the company into liquidation and subsequently cancelled the company’s listing on the exchange in 2020.

SFC Obtains Director Disqualification Orders for Breach of Fiduciary Duties

In a case that demonstrates the consequences of directors’ failing to properly fulfill their fiduciary duties, the SFC obtained disqualification orders in the Court of First Instance against two former directors of Long Success International (Holdings) Limited: Mr. Hu Dongguang and Mr. Guo Wanda. The commission disqualified the two from serving as directors or being involved, directly or indirectly, in the management of any corporation in Hong Kong for a period of three years after they admitted to breach of their fiduciary duties and common law duties to act in the interest of the company and to exercise due and reasonable skill, care and diligence in the course of acting as directors of Long Success.

Specifically, Mr. Hu and Mr. Guo admitted that they had allowed the former chairman and executive director of Long Success to exercise domination and control of Long Success and its board of directors for their personal advantage or other ulterior purposes. Further, they admitted that they neglected to exercise their duties as directors of Long Success by (i) approving a confirmation letter in March 2011 to defer the payment owed to Long Success under a profit guarantee concerning an acquisition, which was prejudicial to Long Success, and (ii) failing to monitor or induce the profit guarantee.

The SFC also commenced legal proceedings against other former directors of Long Success, which are ongoing.

HKEx Censures Directors Failure To Cooperate With Investigations

Two recent cases highlight the importance for directors, even after they cease acting as directors, to cooperate with HKEx inquiries and investigations and to comply with the obligation to notify HKEx of changes to their contact details.

In the first case, HKEx censured current and former directors of Youyuan International Holdings Limited for failure to respond to HKEx inquiries. One of the directors failed to provide any submission to the exchange despite repeated reminders, thereby breaching his commitment to HKEx to cooperate in any investigation. Other directors also failed to respond or to notify the exchange of changes to their contact information, thereby breaching their undertakings to HKEx to cooperate in any investigation and/or provide their most current and accurate contact details for a period of three years from the date on which they cease to be directors.

In the second case, HKEx censured five former directors of Summi (Group) Holdings Limited for failure to cooperate with the exchange’s investigations, which were intended to examine whether the directors had breached the Listing Rules. The directors did not respond to HKEx’s investigation letters and reminder letters, and therefore breached their director’s duties to the exchange to (i) cooperate in any investigation conducted by HKEx, (ii) promptly and openly answer any questions addressed to them, and (iii) provide up-to-date contact details to HKEx for three years after they cease to be directors. This constituted a breach of the Listing Rules. HKEx stated that the retention of office by the relevant directors would have been prejudicial to the interests of investors.

Both cases emphasize the importance of directors cooperating with HKEx investigations-related requests in a prompt and open manner and maintaining accurate contact information with the exchange. The cases also highlight that a director’s obligation to provide information requested by the exchange does not lapse when his or her service as a director ends or if the company is in liquidation. Any failure by directors to comply with HKEx requests in connection with an investigation of possible Listing Rule breaches without a reasonable excuse will result in the imposition of severe sanctions.

HKEx Censures and Criticizes Directors of Huiyin for Failed Acquisition

Inadequate documentation and procedures, including inadequate due diligence, in connection with an acquisition recently resulted in HKEx sanctioning directors of a listed company. The case highlights the need for listed companies to retain proper professional advisors when engaging in acquisition transactions.

Huiyin Holdings Limited undertook two acquisitions that involved both a redemption right if one of the targets was unable to list on the NASDAQ exchange and a personal guarantee from the vendor. Although the acquisitions were completed, an HKEx investigation found that Huiyin had relied on inadequate due diligence documentation on the targets and that the company could not locate key documents relating to the guarantee. Additionally, HKEx could not obtain evidence verifying Huiyin’s ownership of its interest in one of the targets. Further, an internal control adviser engaged by Huiyin highlighted that the company lacked a written comprehensive investment policy and procedures. As a result of these various failures, Huiyin’s auditors issued an audit disclaimer in Huiyin’s annual results for the year ending June 30, 2017. This disclaimer was issued within 12 months of the acquisition, at which point Huiyin was unable to confirm with certainty whether the acquisition was properly completed. Huiyin recorded an impairment of the full amount of the acquisition in its FY2018 results, and the write-off constituted approximately 65% of Huiyin’s total loss for the FY2018.

HKEx considered these breaches to be serious, and imposed sanctions and directions on seven former directors for failure to apply the degree of skill, care and diligence reasonably expected of a person of their knowledge and experience and holding their office with the issuer, and for failure to comply with the Listing Rules and/or to cooperate with HKEx’s investigation.

HKEx Censures Tech Pro in Connection With Joint Venture Investment

HKEx recently sanctioned a listed company and its management for failure to properly manage its interest in a joint venture company.

In March 2014, Tech Pro Technology Development Limited acquired a 50% interest in a joint venture (JV) engaged in the business of property subleasing. Two of Tech Pro’s directors acted as the company’s representatives in the transaction. However, Tech Pro and its directors were found to be overly reliant on the JV partner, were unable to obtain control or participate in the operations of the JV, and did not ensure that Tech Pro took adequate steps to protect its interests. Tech Pro’s monitoring of the JV’s operations, which HKEx found to be insufficient and ineffective, resulted in losses to the JV’s assets. Tech Pro’s representatives in the JV also failed to raise objections to questionable dividend arrangements in relation to the JV partner. This resulted in the JV withholding dividend payments to Tech Pro, a form of financial assistance which Tech Pro did not properly disclose.

As a result, HKEx censured Tech Pro for the late disclosure of this financial assistance, and for the related delayed publication of financial results and reports. HKEx also censured seven of the former directors for (i) failure to implement effective risk management and internal control procedures to monitor the operations of the JV or safeguard its assets, (ii) failure to act honestly and in good faith in the interests of Tech Pro as a whole, (iii) failure to discharge their responsibilities under the Listing Rules and (iv) failure to effect Tech Pro’s compliance with the Listing Rules in breach of their undertakings to HKEx. The exchange noted that the retention of office by the two directors who represented Tech Pro in the JV would have been prejudicial to the interests of investors, and directed the relevant directors to attend training.

Market Misconduct Tribunal Sanctions COL and Its Directors for Late Disclosure of Inside Information

A recent case reminds listed companies of their obligation under the Securities and Futures Ordinance to disclose inside information — including positive information — to the market as soon as reasonably practicable.

In the case, the Market Misconduct Tribunal (MMT) fined China Medical & HealthCare Group Limited, formerly known as COL Capital Limited, and six of its former and current directors a total of HK$4.2 million for failing to disclose inside information as soon as reasonably practicable. The tribunal also disqualified one former and one current director from serving as listed company directors for eight and six months, respectively.

The inside information in question was related to COL’s significant investment gains from trading in shares of ChinaVision Media Group Limited, now known as Alibaba Pictures Group Limited, and the impact of those gains on COL’s March 2014 profit figures. The directors became aware of this information through an internal financial report in April 2014, but did not ensure that the information was disclosed to the public until the company issued a positive profit alert in September 2014.

The tribunal found that, as a result of the five-month delay, COL failed to disclose the inside information as soon as reasonably practicable and thus breached the inside information disclosure requirement under the Securities and Futures Ordinance.

MMT Sanctions ENN Energy’s Former CFO for Insider Dealing

The MMT found Mr. Cheng Chak Ngok, a former executive director, chief financial officer and company secretary of ENN Energy Holdings Limited (ENN), to have engaged in insider dealing regarding shares of China Gas Holdings Limited.

The tribunal determined that Mr. Cheng completed transactions involving China Gas shares in 2011 while in possession of nonpublic information about ENN Energy’s preconditional voluntary general offer to acquire shares of China Gas, which was material to the share price of China Gas. Mr. Cheng then sold the shares after the announcement of the takeover offer at a profit of around HK$3 million.

In determining its sanctions, the MMT ruled that Mr. Cheng is “unfit to be a director of any corporation, whether listed or not” and that he “abused his expertise and breached the trust and confidence which he enjoyed.” The tribunal thus issued orders banning him from dealing in any securities in Hong Kong and disqualifying him from serving as a director or taking part in the management of a listed corporation, in each case for 54 months.

The MMT also found that Mr. Cheng’s “misconduct brought Hong Kong into disrepute as a financial centre,” and further ordered disgorgement of profits arising from the insider dealing and that he pay the costs and expenses of the government and of the SFC. Additionally, the tribunal referred the matter to the Hong Kong Institute of Certified Public Accountants with a recommendation to take disciplinary action against Mr. Cheng, who was a qualified accountant.

HKEx Criticizes Chairman of China Metal for Breach of Model Code

Another recent enforcement action emphasizes that directors of listed companies who deal in the shares of the company are subject to the Model Code for Securities Transactions by Directors of Listed Issuers, and any breaches will be subject to disciplinary proceedings by HKEx.

In the case, HKEx criticized Mr. Yu Jian Qiu, the executive director and chairman of China Metal Resources Utilization Limited, for selling shares during a blackout period and without notifying the board or obtaining the designated director’s approval. Mr. Yu’s action constituted a breach of the Model Code and his undertaking to comply with the Listing Rules to the best of his ability.

The Model Code prohibits directors from dealing in securities on any day on which the listed issuer’s financial results are published and during the period of (i) 60 days immediately preceding the publication of the annual results announcement and (ii) 30 days immediately preceding the publication of the interim or quarterly results announcement. The Model Code also requires the chairman of a listed issuer to first notify the board or the designated director to obtain a dated written acknowledgment before dealing in any securities. Additionally, HKEx directed Mr. Yu to attend training.

![]()

For further information, please contact:

Paloma Wang, Partner, Skadden

paloma.wang@skadden.com