In February 2026, the China Securities Regulatory Commission (CSRC) issued the Measures for the Supervision and Administration of Information Disclosure of Private Investment Funds (the “Information Disclosure Measures”), which will come into effect on September 1, 2026. The Information Disclosure Measures constitutes an important ancillary rule for the implementation of the Regulation on the Supervision and Administration of Private Investment Funds (the “Private Fund Regulation”). Compared with the previous regulatory framework, which was based on industry self-regulatory rules, the Information Disclosure Measures improves the regulatory regime in terms of legislative hierarchy, scope of application, disclosure requirements and legal liabilities, and impose clearer and more stringent information disclosure obligations on private fund managers.

By summarizing the key provisions of the Information Disclosure Measures, this briefing analyzes several issues requiring particular attention by private securities fund managers.

I. Elevation of the Legal Hierarchy of the Rules

Previously, information disclosure of private funds was mainly governed by self-regulatory rules issued by the Asset Management Association of China, such as the Measures for the Administration of Information Disclosure of Private Investment Funds. The newly issued Information Disclosure Measures is promulgated by the CSRC in the form of departmental rules, thereby elevating the legal hierarchy of the provisions. The superior legal basis of the Information Disclosure Measures has been adjusted from the Interim Measures for the Supervision and Administration of Private Investment Funds to the Private Fund Regulation. The elevation of the legislative hierarchy means that information disclosure requirements have been upgraded from self-regulatory rules to administrative regulation, and regulatory enforcement is expected to be strengthened accordingly.

II. Expansion of the Scope of Applicable Entities

The Information Disclosure Measures expands the scope of applicable entities. In addition to private fund managers and custodians, private fund distribution agencies and other private fund servicing institutions are also brought within the scope of information disclosure supervision, thereby covering whole process of private fund operations.

The Information Disclosure Measures also introduces a new requirement that shareholders, partners and actual controllers of private fund managers shall cooperate in fulfilling information disclosure obligations. This provision strengthens compliance obligations after see-through to the equity ownership of private fund managers.

With respect to custodians, the Information Disclosure Measures references the institutional framework of the Measures for the Administration of Custody Business of Securities Investment Funds, which is applicable to public funds. It integrates and clarifies the information disclosure obligations of custodians and requires custodians to conduct necessary verification of information such as the financial status of funds. We note that the Measures for the Supervision and Administration of Custody Business of Commercial Banks (Trial), which came into effect on February 1, 2026, impose same requirement on commercial banks that provide custody services.

III. Introduction of “Timeliness” Requirement and Voluntary Disclosure

The Information Disclosure Measures provides that disclosure shall follow the principles of truthfulness, accuracy, completeness and timeliness. Timeliness has been included as a disclosure standard, emphasizing that managers should disclose information to investors within a reasonable period so that investors are kept informed of the funds’ operation.

The Information Disclosure Measures establishes a model combining mandatory disclosure and voluntary disclosure. In addition to the information required to be disclosed by law, managers may also conduct voluntary disclosures as needed. Such voluntary disclosures shall still comply with the fundamental principles of truthfulness and accuracy, shall not contain misleading statements, and shall not constitute disguised false publicity.

IV. Increased Disclosure Frequency with Extended Deadlines for Quarterly Reports

The Information Disclosure Measures does not require private securities investment funds to submit monthly reports. However, it requires that the disclosure frequency of the share net asset value and cumulative share net asset value of open-ended private securities investment funds shall not be lower than the frequency of fund opening. This means that, upon the implementation of the Information Disclosure Measures, private securities fund managers shall disclose the share net asset value and cumulative share net asset value of all their open-ended private securities funds to investors in accordance with the opening frequency stipulated in the fund contract, regardless of the fund’s asset size. For example, if the fund contract provides that the fund opens once per week, the net asset value information shall be disclosed to investors on a weekly basis. Closed-ended private securities investment funds shall disclose fund net asset value information to investors at least once per quarter.

The Information Disclosure Measures adjusts the disclosure deadline for quarterly reports, extending it from the previous 10 working days to one month. This adjustment, to a certain extent, alleviates the time pressure on managers in preparing information disclosures.

The Information Disclosure Measures specifies that when a major event occurs, the manager shall prepare an ad hoc report and disclose it to investors within five working days from the date of the occurrence of the major event. Compared with the previous principle-based requirement of timely disclosure, the new rules have introduced a clear time limit.

V. Introduction of See-through Disclosure and Expanded Major Event Disclosure Requirements

With respect to the content of periodic reports, the Information Disclosure Measures introduces a see-through disclosure requirement. Where private securities investment funds invest in other private funds or lawfully launched asset management products (excluding publicly offered securities investment funds), the manager shall disclose not only the information on its own invested assets, but also the investment path of each layer and the underlying assets identified through see-through. For fund-of-funds (FOF) products, the regulatory authorities may further refine requirements through additional rules in the future.

With respect to the content of ad hoc reports, the Information Disclosure Measures add several scenarios for major events disclosure, including the convening of fund unit holder meetings, partner meetings or shareholders’ meetings and the matters resolved thereby. If a major adverse event occurs in respect of a fund’s primary investment target and has a material negative impact on investors’ rights and interests, the manager shall, in the ad hoc report, explain the reasons and provide risk warnings to investors. We understand that managers may assess whether a major adverse event exists by considering whether changes in the primary investment target may materially affect the fund’s net asset value, investment returns, exit arrangements, capital safety or other aspects.

Currently there is no mandatory audit requirement for contractual-type private securities funds with custodians. The Information Disclosure Measures specifies that where a private securities fund falls into any of the following categories, its annual financial statements shall be audited by an accounting firm filed with the CSRC: (i) the fund mainly invests in illiquid assets; (ii) the fund mainly invests in derivatives; (iii) the fund mainly invests in overseas assets (excluding direct investments in overseas standardized assets); (iv) the fund mainly invests in private funds managed by other private fund managers; or (v) other circumstances prescribed by the CSRC. This means that QDLP funds adopting a feeder-master fund structure will be required to conduct annual audits after the Information Disclosure Measures takes effect.

VI. Upgrading Internal Governance and Record Retention Requirements

The Information Disclosure Measures requires private fund managers and custodians to establish and improve information disclosure management policies. These policies shall not only include mechanisms for handling investor inquiries relating to information disclosure but shall also introduce a policy specifically for the management of non-public information. While responding to reasonable investor information requests in a timely manner, managers shall also ensure that the entire process of information transmission remains secure and controllable.

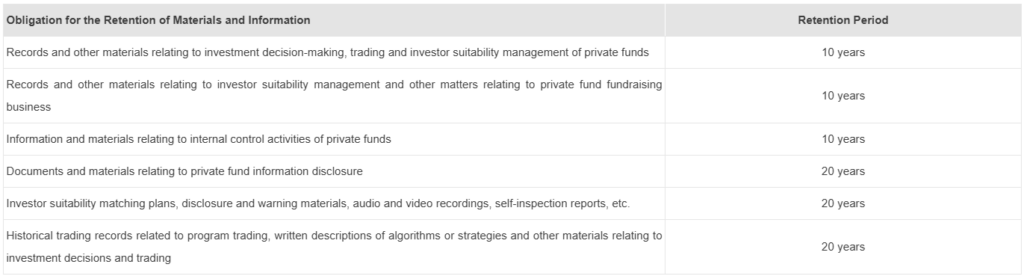

The Information Disclosure Measures extends the minimum retention period for information disclosure materials from 10 years to 20 years after the completion of fund liquidation and requires dedicated departments and senior management personnel designated responsible for record management. This significantly increases the requirements for information retention and internal management.

After the Information Disclosure Measures takes effect, the obligations and retention periods for private fund managers regarding the preservation of information and records will be as follows:

VII. Administrative Liability for Information Disclosure Violations

The Information Disclosure Measures contains a separate chapter on supervision and legal liabilities, specifying that the CSRC and its dispatched offices have the authority to supervise the information disclosure activities of private fund managers, custodians, distribution agencies and servicing institutions. Regulatory authorities may impose administrative supervisory measures such as ordering rectification, conducting regulatory interviews and issuing warning letters in accordance with the law. Violations of information disclosure obligations may also be subject to administrative penalties pursuant to the Private Fund Regulation and other applicable laws and regulations.

Prior to this, administrative penalties for violations relating to private fund information disclosure were mainly imposed by the CSRC pursuant to Article 56 of the Private Fund Regulation and Article 38 of the Interim Measures for the Supervision and Administration of Private Investment Funds. The issuance of the new measures further improves the legal basis for penalties and regulatory enforcement actions.

VIII. The “New-Old Cut” Principle

With respect to the implementation arrangements, the Information Disclosure Measures adopts the regulatory principle of “New – Old Cut”. From September 1, 2026, when the Information Disclosure Measures officially takes effect, newly filed private funds shall comply with the provisions of the Information Disclosure Measures regarding fund contracts and other terms. For existing private funds, it is not mandatory to amend the fund contract immediately. However, in case of any change to the fund contract in this regard, the changed sections are required to comply with the Information Disclosure Measures.

IX. Next Step – Our Recommendations

Private fund managers are recommended to complete the following preparatory work before the Information Disclosure Measures comes into effect:

- Review the information disclosure provisions in existing fund contracts, or update fund contract templates together with custodians, to ensure compliance with the Information Disclosure Measures;

- Revise and improve information disclosure policies, designate specialized departments and senior management personnel responsible for information disclosure matters, confirm the workflow and internal control mechanisms to ensure information disclosure is truthful, accurate, complete and timely, introduce mechanisms for handling investor inquiries on information disclosure, revise retention periods for disclosure-related materials, and introduce accountability mechanisms for failure to disclose information as required;

- Establish a non-public information management policy;

- Improve the management and preservation of information disclosure archives;

- Confirm whether the private funds under management fall within the scope requiring mandatory audits.