10 January, 2018

A legal battle can be one of the most business-disruptive challenges a company faces. When confronted with potential costly litigation, it is key that a company adopts a vigilant approach towards its accounting, and critically that when nancial trouble starts it takes immediate action to avoid an otherwise inevitable trajectory towards insolvency.

Of course, a company should always be in control of its finances and seek advice when needed; not only in exceptional circumstances.

ICAEW survey

Insolvency Practitioners questioned in a recent ICAEW survey felt that the top three reasons preventing companies from seeking professional advice earlier were: worry about loss of control in the final outcome (57%), lack of knowledge of options (52%), fear of impact on family and lifestyle and a concern over costs (both 41%), too often resulting in inaction.

The negative stigma attached to business failure – or the impending threat of it – must change.

Having adopted the British approach of pretending everything is just fine when all is failing, many businesses have fallen into avoidable insolvency.

We believe that a change in attitudes is critical to avoid corporate insolvencies – substantially increased in number – by confronting business issues, rather than being ashamed of them. With the early help of restructuring and insolvency practitioners, a review of processes or management is possible, which in turn can salvage many businesses, bringing them back into profit.

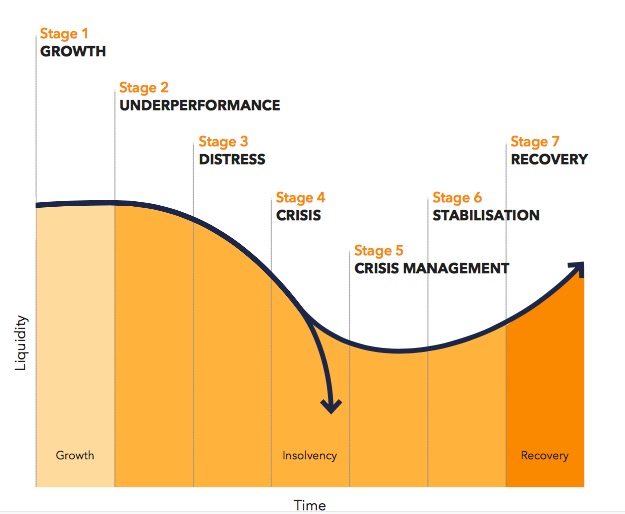

Our new insolvency and restructuring guide shows the different stages of a business with problems, with two outcomes: insolvency or recovery (see graph below).

Please click on the graph to enlarge.

Recognising the warning signs

Tax liabilities such as NI, PAYE and VAT repayments can often be a key element in losing control of company finances. Often seen as a non-critical supplier – as opposed to the purchase of legal or wage bills – HMRC can sometimes end up being a large stakeholder in failing businesses with numerous debts to recoup. By gaining timely advice from tax practitioners at the early stages many businesses could avoid potential insolvency.

Many businesses approach HMRC to secure a Time to Pay arrangement, staggering payments and enabling owner/managers to regain control of their nances. Demonstrating that the cash-flow crisis was a one-off caused by extenuating circumstances, such as legal challenges, is suficient to gain such terms from HMRC. Too many businesses however, see this as an easy way to keep working capital in the business and only deal with the symptom, not the cause of the cash-flow issue. Defaulting on Time To Pay instalments bear a costly consequence.

Recovery or insolvency?

When a business struggles to pay HMRC on a due date, the alarm bells should begin ringing. Management must ask themselves why it is they can’t pay, and objectively review their liquidity issues. Is it just the legal bills they are facing or is the problem more endemic? It’s critical to establish if these are short-term cash-flow issues or more substantial problems at the route of the company’s accounts. This will help establish the nature of the re-financing needed.

If the company is loss-making it must look at improving the bottom line – possibly through an increase in sales or prices, or by reducing costs or manpower within the business. In practice, it is not uncommon to see a business shrink as a foundation to any turnaround plan, enabling the business to free up much needed working capital, whilst at the same time refocussing on customers and activities that are pro table, and possibly move to recovery.

If all efforts have been made to bring the business out of its decline without success then it is time to resort to insolvency procedures.

Options such as an accelerated merger and acquisition process or going into trading administration, disposing of assets and the business as a going concern may provide an acceptable result for creditors but in these cases, it will mark the end of the business for the owners.

One of the more exible arrangements is a Company Voluntary Arrangement (CVA) which enables owners to retain day to day control whilst returning a more beneficial return to creditors, albeit over time. A number of key ingredients must be in place:

The company’s restructure under a CVA must demonstrate it would deliver a better result for creditors.

They must achieve the buy-in of investors and the owner/manager(s) to be entirely open to administering the necessary changes to restore pro tability.

The support of 75% by value of the company’s unsecured creditors must be secured, in many cases the most influential of which is HMRC.

The licensed insolvency practitioner can then become the conduit with HMRC in the formal role of supervisor, acting as a go-between with the company and its creditors. Critically though, this option is really only open to businesses that face up to their problems early – if left too late then it is most likely that an administration or voluntary liquidation will be the only remaining option available to them.

How can lawyers help?

The greatest help legal advisers can provide to a business that has entered the decline curve is to help their clients take an objective look at the state of their business. They can also ensure the company knows which early signs of problems to look for. As soon as the ‘zone of crisis’ is entered the company must seek help to avoid insolvency.

The difference between businesses that survive and thrive and those that fail is how well they manage such difficulties. If they do this well, it is possible to move away from insolvency, towards crisis management, stabilisation and finally onto recovery.

By Bob Pinder, Insolvency Director, the Institute of Chartered Accountants in England and Wales.

For further information, please contact:

Ruth Stackpool-Moore, Director of Litigation Funding / Head of Harbour Hong Kong

ruth.sm@harbourlf.com