22 October, 2018

We are moving towards a data centric world, and “data is the new oil”[1]. And few would disagree that a key debate today in finance is ‘trust and privacy vs. using data for business growth’. As modern day businesses look to adapt themselves to generate revenue from customer related data, regulators across the world are grappling with the formulation of effective laws to regulate the data-driven economy. Given the relative novelty of the concept, regulators are reflecting on fundamental questions such as the right to privacy, property rights over data andthe right to use the collected data.

In India, the Reserve Bank of India (“RBI”) has been fairly forward looking, by passing various regulations and constituting a host of committees to address issues ranging from cyber security to customers data protection norms.[2] In almost all its regulations, RBI has adopted a data privacy framework similar to the one advocated by the Justice BN Srikrishna Committee in its Personal Data Protection Bill, 2018 (“DP Bill”) – an amalgamated framework consisting of consent-and-notice and the vesting of certain rights with the originators of such information.[3] Undoubtedly, the DP Bill will have an impact on the manner in which data is collected, processed and shared by the financial industry. With this as the background, the authors seek to analyse the impact of the DP Bill on businesses engaged in the financial sector.Key Concepts

The DP Bill recognises the need to protect and regulate the use of personal data. It creates fiduciary relationships by defining individuals as Data Principals and any entity that “processes” their personal and/or sensitive personal data as Data Fiduciaries.

- “Personal Data” (PD) has been defined to mean any data that identifies or can identify an individual.

- “Sensitive Personal Data” (SPD) means personal data, along with financial data, biometric data, etc.

- “Processing” has been defined in broad brushstrokes, to make any activity relating to PD or SPD, such as collecting, sharing, storing, altering, indexing, disclosing etc.[4] While there are exceptions to receipt of consent in the DP Bill, in the financial sector data may typically be processed by Data Fiduciaries (DF) or Data Processors (DP) with (a) issuance of a notice by a DF to an individual for such purpose, and (b) followed by receipt of consent from the individual. [5] The processing notice has to be fairly extensive and must disclose, among other things, the purpose of processing, the entities with which data will be shared and details of the grievance redressal officer of the Data Fiduciary.

- Consent from individuals: a layered concept of consent is proposed by the DP Bill, as depicted below:

Please click on the image to enlarge.

Data Localisation and Cross-Border Data Transfers: More Compliance Costs?

Transfers

Under Section 2 of the DP Bill, DP Bill will apply upon (a) processing of data within India and (b) if such processing is by entities incorporated or created under Indian law. But, for entities that do not have a ‘presence’ in India, the DP Bill will apply for processing undertaken ‘in connection with’ any business in India or processing involving profiling of individuals resident in India. Consider three scenarios –

- XYZ Bank, a foreign Bank, has a branch office in India which provides certain services directly to Indian clients;

- XYZ Bank, a foreign Bank, has a branch office in India, which merely does certain kinds of data aggregation and profiling work of only XYZ’s foreign clients; and

- ABC Bank Limited, an Indian Bank, has an offshore branch office. This branch office sends data of offshore clients to its Indian office, wherein certain kinds of data aggregation and profiling work is undertaken.

Scenario 3 will definitely attract the DP Bill, as the DF is incorporated in India and the processing is taking place in India. However, the analysis is not as straightforward in the case of Scenarios 1 and 2. An Indian branch office of a foreign bank is not an entity incorporated in India, but it can be argued that this branch office represents ‘presence’ of the foreign bank in India, and as a consequence, the relevant foreign bank (along with its branch office) may fall outside the scope of Section 2 of the DP Bill.[6]

The DP Bill also seeks to regulate cross-border transfer of personal data by mandating that any such transfer, on the basis of standard business contracts, will require the consent of the relevant Data Principals, provided such contracts have been approved by the DPA.

Localisation

Another aspect that may require some deliberation is data localisation. In April 2018, when RBI issued a notification mandating all payment systems to store all data relating to their business only in India, various market participants argued that apart from compliance costs, ‘data restriction’ may also prejudice India’s global competitiveness in the knowledge industry.[7] However, the DP Bill also takes a similar stance, and requires a serving copy of all data to which the DP Bill applies to be stored in India by the DF.

Such data storage and transfer restrictions may result in restructuring of business processes and increase in compliance costs for banks and financial institutions having a cross-border presence.

KYC: an implied amendment

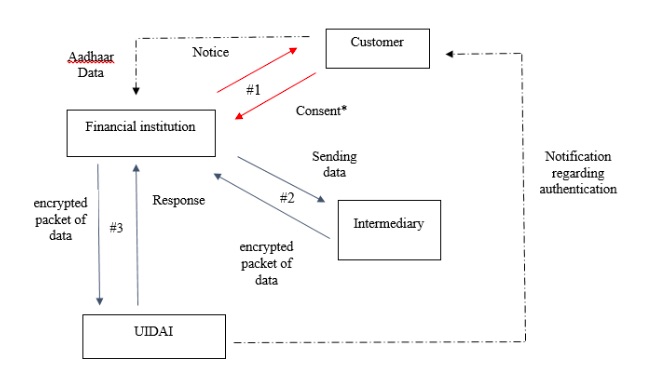

Since the introduction of Aadhaar, most banks and financial institutions have moved towards KYC processes that are Aadhaar-centric.[8] Prior to the introduction of the DP Bill and the Supreme Court’s judgment in the Aadhaar case[9], the process of Aadhaar-based e-KYC verification was as below:

Please click on the image to enlarge.

* Explicit consent will have to be sought from DPs.

However, owing to the Supreme Court’s judgment now, there is uncertainty regarding the permissibility of Aadhaar-based e-KYC by banks and financial institutions.

Cybersecurity: adoption of “privacy-by-design”

The DP Bill adopts the principle of “privacy-by-design”, which requires Data Fiduciaries to (a) design policies with a view to prevent potential harm to individuals, (b) protect privacy at every stage till data deletion, and (c) carry out of transparent processing.[10] Accordingly, cybersecurity processes of banks and financial institutions may require a review and overhaul.

Recovery of loans: right to privacy implications

Certain recovery strategies implemented by banks and financial institutions, such as the right to publish a defaulter’s personal data in newspapers, has often been litigated over.[11] This issue, which has seen conflicting judicial opinions, should be laid to rest by the DP Bill. The DP Bill would not prohibit such actions, but would make them subject to the notice-and-consent mechanism. [12]

Points to ponder

A fair distance remains to be covered before the data protection framework envisioned in the DP Bill becomes a reality. The rules and regulations relating to implementation of the various substantive provisions are yet to be prescribed.

Having said that, if the DP Bill (and its related rules) is passed as law without significant changes, it will result in the introduction of a comprehensive ‘notice-and-consent plus rights-based framework’ – something that will strike a much needed balance between present day data driven businesses and ‘right to data protection’. The old ways of unfettered collection and storage of data by business in the financial sector will change. Market participants will have to invest in new technology, set-up new compliance processes, revise customer facing documentation and overhaul their knowledge sharing processes.

Though established players in the financial industry may find it easy to cope with the changes in law and may already be ahead of the curve, it will be interesting to see how India’s burgeoning fintech companies will adapt to the same.

For further information, please contact:

Avinash Umapathy, Partner, Cyril Amarchand Mangaldas

avinash.umpathy@cyrilshroff.com

[1] See generally, “The World’s Most Valuable Resource is Data, not Oil” at https://www.economist.com/leaders/2017/05/06/the-worlds-most-valuable-resource-is-no-longer-oil-but-data

[2] See for example, the report of the Housing Finance Committee constituted in 2016 (available here) and the report of the Working Group on Information Security, Electronic Banking, Technology Risk Management and Cyber Frauds constituted in 2010 (available here).

[3] The full text of the DP Bill can be accessed here. Interestingly, the Housing Finance Committee, in its report, advocated for adopted of a purely rights-based approach to data protection. The rationale for the same was the ability to procure true informed consent in a world of constant automation and profiling. The author of this section of the Committee’ report, Rahul Matthan, has outlined reasons for adoption of a rights-based approach to data protection in his discussion paper for Takshashila Policy Research here, as well.

[4] Section 3(32) of the DP Bill defines processing as –

“an operation or set of operations performed on personal data, and may include operations such as collection, recording, organisation, structuring, storage, adaptation, alteration, retrieval, use, alignment or combinations, indexing, disclosure by transmission, dissemination or otherwise making available, restriction, erasure or destruction”

[5] Under Section 8 of the DP Bill, this includes the type of data collected, the purposes for which is being collected, the persons with whom the data will be shared, information on any cross border transfer of the data and details of the grievance redressal officer appointed by the Data Principal/Data Processor.

Further, there are other grounds of processing of personal data, which don’t require full adherence to notice-and-consent. These grounds are, processing of data by courts, processing of data during medical emergencies, and processing of data for reasonable purposes notified by the Data Protection Authority. Further, processing of personal data for reasonable purposes, inter alia, include processing in relation to whistle blowing, credit scoring and recovery of debt.

[6] Section 2 of the DP states that –

“Application of the Act to processing of personal data.—

(1) This Act applies to the following—

(a) processing of personal data where such data has been collected, disclosed, shared or otherwise processed within the territory of India; and

(b) processing of personal data by the State, any Indian company, any Indian citizen or any person or body of persons incorporated or created under Indian law.

(2) Notwithstanding anything contained in sub-section (1), the Act shall apply to the processing of personal data by data fiduciaries or data processors not present within the territory of India, only if such processing is —

(a) in connection with any business carried on in India, or any systematic activity of offering goods or services to data principals within the territory of India; or

(b) in connection with any activity which involves profiling of data principals within the territory of India.

(3) Notwithstanding anything contained in sub-sections (1) and (2), the Act shall not apply to processing of anonymised data.” (emphasis supplied)

This shall be discussed in detail in our next blog post.

[7] RBI circular bearing no. RBI/2017-18/153 on Storage of Payment System Data, dated April 6, 2018. See also https://economictimes.indiatimes.com/news/economy/policy/rbi-note-on-data-localisation-raises-hackles-in-the-us/articleshow/63966786.cms

[8] Know Your Customer (KYC) Directions, 2016.

[9] The judgment can be accessed from here.

[10] See Section 29 of the DP Bill. Further, a general overview of the concept of “privacy-by-design” can be found here

[11] The Calcutta High Court (in SBI v. Ujjal Kumar Das AIR 2016 Cal 281) and the Kerala High Court (in Venu v. SBI MANU/KE 0723/2013) are not in favour of allowing this method of recovery, while Madras High Court (in K.J. Doraisamy v. State Bank of India (2006) 4 MLJ 1877) and the Madhya Pradesh High Court (in Archana Chowhan v. State Bank of India AIR 2007 MP 45) have permitted this method of recovery.

[12] However, in the case of state-owned or state-run banks, such publication and dissemination of the borrower’s personal data would also be subject to constitutional law considerations of the right to privacy under Article 21. In this regard, see for example the judgment of the Calcutta High Court in the case of SBI v. Ujjal Kumar Das AIR 2016 Cal 281.