Setting Up A Fund Management Company In Malaysia: The Legal And Compliance Requirements.

The Evolving Landscape of Fund Management Industry in Malaysia

The Malaysian fund management industry has demonstrated remarkable resilience and growth. Data from 2024 highlights that the industry’s Assets Under Management (“AUM”) exceeded RM 1.1 trillion, a significant leap from RM 975.5 billion in 2023. This upward trajectory is not merely a statistical anomaly but reflects a broader deepening of the capital market, which now stands at RM4.2 trillion.

This expansion aligns with a key component of Malaysia’s national economic strategy. The Securities Commission Malaysia (“SC”) highlighted this vision through the Capital Market Masterplan 3, a five-year plan aimed at creating a capital market that is more relevant, efficient, and diversified.[1] Notably, the government has announced that this AUM growth is attributed to strong demand, further supported by recent budgets initiatives such as the Single-Family Office Incentive Scheme and the ASEAN Business Entity status. As of late 2025, the Single-Family Office Incentive Scheme has approved six family offices with nearly RM 400 million in AUM, targeting RM 2 billion by the end of 2026. These initiatives are specifically designed to attract private wealth and skilled talent.[2]

With sustained demand and government policies designed to attract capital, the environment remains favourable for new entrants. To make full use of this opportunity, investors must understand the licensing structure and regulatory requirements that govern the industry. This article sets out the key legal framework and the practical considerations involved when establishing a Fund Management Company (“FMC”) in Malaysia.

Licensing Requirement of Fund Management Companies

The establishment and operation of an FMC is governed primarily by the Capital Markets and Services Act 2007 (“CMSA 2007”). Schedule 2 of the CMSA 2007 defines fund management as the undertaking, on behalf of any other person, the management of a portfolio of securities or derivatives, or the management of an asset in a unit trust scheme. Consequently, any entity performing fund management activities must obtain a Capital Markets Services Licence (“CMSL”) issued by the SC.

Before filing a license application, an applicant must decide which licensing pathway best suits their intended business model. The SC’s Licensing Handbook sets out two primary routes, each with different capital requirements and operational limitations.

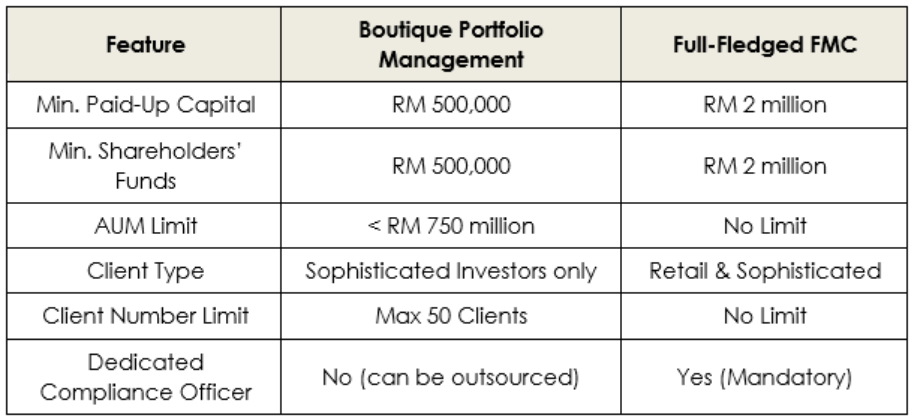

The Full-Fledged Fund Management Company Licence

This category represents the standard institutional licence. It permits for the broadest scope of business operations, allowing holder to manage unlimited assets for both retail and sophisticated investors.

To operate at this level, the SC imposes rigorous financial and human capital requirements. The applicant must maintain a minimum paid-up capital and shareholders’ funds of RM 2 million at all times. Structurally, the compliance standards are strict. The FMC must appoint a licensed director who holds a Capital Markets Services Representative’s License and has a minimum of 10 years of relevant experience. Furthermore, it is mandatory to appoint a dedicated and SC-registered compliance officer. The officer must meet minimum competency requirements, such as possessing a relevant degree with three years of experience and passing the relevant SC licensing examinations.[3]

The Boutique Portfolio Management Company Licence

Recognising the need for a more accessible entry point for niche players, the SC introduced the Boutique Portfolio Management license. This category significantly lowers the financial barrier, requiring a minimum paid-up capital and shareholders’ funds of only RM 500,000. Furthermore, a licensed director is not mandatory, and the applicant is permitted to outsource the compliance function to a qualified provider, subject to the SC’s prior approval.

However, this lower entry barrier comes with strict operational restrictions, as follows:

a. The company cannot manage assets exceeding RM 750 million;

b. Services must be restricted solely to sophisticated investors (high-net-worth individuals or corporates); and

c. The FMC is limited to a maximum of 50 clients.

Regardless of the pathway chosen, all applicants (both the corporate entity and its key personnel) must meet the SC’s fit and proper criteria. This involves a thorough assessment of an applicant’s probity, financial integrity, reputation, character and ability to perform their functions efficiently, honestly and fairly.

The Licensing Process: Application, Timelines and Costs

For prospective entrants, navigating the procedural aspects of licensing is as significant as meeting the capital requirements.

The Application Process

All applications for a CMSL must be submitted through the SC’s Electronic Application System (EASy). The submission requires a comprehensive business plan, including corporate profiles, organisational structures and five-year financial projections. Crucially, the applicant must demonstrate that its directors, chief executive, and key management personnel meet the fit and proper criteria set out in Section 64 of the CMSA 2007.

Timelines

The SC is committed to a client charter of six weeks for the processing of a new CMSL application, provided the submission is complete and meets all fit and proper criteria.[4] However, applicants should factor in additional time for the SC to conduct readiness audits or interviews to assess the competency of key personnel.

Application Fee

The fee for a new CMSL application is RM 2,000.[5]

Costs and Annual Licence Fees

Investors must also account for the revised fee structure under the Capital Markets and Services (Fees) Regulations 2025, which comes into operation on 1 January 2026. The fee structure is moving towards an AUM-based calculation (e.g., 0.0125% for equities, 0.01% for bonds/mixed assets, 0.0025% for money market/private mandates), with a minimum annual fee of RM 20,000.[6]

Digital Assets and Digital Investment Managers

The growth of financial technology presents new business opportunities for modern FMCs. However, this area requires careful attention because the legal framework differs depending on whether a company wishes to manage digital assets (like cryptocurrencies) or operate as a Digital Investment Manager (“DIM”), typically referred to as a “robo-advisor”.

Management of Digital Assets

Under the Capital Markets & Services (Prescription of Securities) (Digital Currency and Digital Token) Order 2019, digital assets such as digital currencies and tokens as classified as securities. Therefore, FMCs managing these assets must do so through SC-registered Digital Asset Exchanges (“DAX”) such as Luno, HATA Digital, MX Global, SINEGY, and Tokenize.

The SC’s Guidelines on Digital Assets focus mainly on DAX and Initial Exchange Offering (“IEO”) operators. There is limited guidance for traditional FMCs that wanted to manage digital assets as part of a broader investment strategy. Therefore, it is strongly advisable for FMCs to rely on the SC’s broad standards of care, skill and diligence when dealing with these asset classes.[7]

Digital Investment Manager

A DIM is not a new type of asset, but a new method of management. A DIM is a fund manager that provides automated discretionary portfolio management using innovative technology to perform core functions such as risk-profiling, asset allocation and rebalancing.

A DIM does not operate under a separate license category. Instead, it operates as a variation to the existing CMSL for fund management. A new applicant or an existing FMC (either Boutique or Full-Fledged) can apply to the SC to have their license varied to include DIM services. Applicants must satisfy the SC that they possess the necessary digital value proposition, technology capabilities, and necessary expertise.[8] The SC has licensed a number of DIMs to date, including Akru Now Sdn Bhd, Amanah Saham Nasional Berhad, CP Global Fintech Solutions Sdn Bhd (Airo), GAX MD Sdn Bhd (MYTHEO), Kenanga Investment Bank Bhd, Raiz Malaysia Sdn Bhd, StashAway Malaysia Sdn Bhd, UOB Asset Management (Malaysia) Bhd and Wahed Technologies Sdn Bhd.

Our Firm’s Role in Your Success

Setting up a Fund Management Company in Malaysia is a detailed and highly regulated process. The CMSA 2007 and the SC’s guidelines impose specific obligations that apply from the application stage to day-to-day operations. Getting these steps right at the beginning is essential, particularly when choosing between a Boutique or Full-Fledged licence, preparing for the SC’s fit and proper assessment and establishing governance standards that meet statutory duties.

The growth of digital assets and the DIM model also requires careful legal and operational planning, as these areas operate under evolving legal frameworks. In this environment, non-compliance with evolving standards can lead to significant implications for both the company and its directors.

For further information, please contact:

George Law Ngo Jun, Azmi & Associates

george.law@azmilaw.com

- Tengku Zafrul Tengku Abdul Aziz, ‘Capital Market Master Plan 3 (CMP3) Launch’ (Speech at the CMP3 Launch, Kuala Lumpur, 21 September 2021), <https://www.sc.com.my> accessed 20 May 2025.

- Securities Commission Malaysia, ‘Malaysia Gazettes Single Family Office (SFO) Rules’ (Media Release, 6 October 2025).

- Securities Commission Malaysia, Licensing Handbook (SC-GL/LH-2007, revised 14 April 2023) para 4.02(17).

- Securities Commission Malaysia, Licensing Handbook (SC-GL/LH-2007, revised 14 April 2023) para 6.03(3)(a).

- Capital Markets and Services (Fees) Regulations 2025, Regulation 2(2)(a).

- Capital Markets and Services (Fees) Regulations 2025, Schedule 3, Paragraph 7(d).

- Securities Commission Malaysia, Guidelines on Conduct for Capital Market Intermediaries (SC-GL/3-2021, revised 29 March 2024) para 8.01.

- Securities Commission Malaysia, Licensing Handbook (n 3) para 4.02(4B).